- You can save money with 7/1 ARM.

- Make sure you understand the risks and how the payments can change.

- Sometimes you can't sell the property or refinance the loan, so make sure you can afford the payments.

An ARM can be the right choice!

If you sell your house or refinance your loan during the first seven years of your loan, then a 7/1 ARM (Adjustable Rate Mortgage) can save you money. Your loan, based on a 30-year payment schedule has a lower interest rate than a 30-year FRM (Fixed Rate Mortgage) and lower monthly payments.

However the 7/1 ARM carries the risk of a higher interest rate and higher payment after the initial period. If you cannot refinance or pay off the loan, then your overall costs may be higher than a fixed rate mortgage.

An adjustable rate mortgage is more complex than a fixed rate mortgage. Before you choose a loan understand the risks and benefits. Learn about:

- 7/1 ARM terminology

- Monthly Payments – Different Scenarios

- Choosing an ARM

7/1 ARM Terminology

The interest rate and monthly payment of a 7/1 ARM is set as follows:

- Initial Period: In a 7/1 ARM the interest rate is fixed for an initial period of 7 years. (The interest rate for a 5/1 ARM is 5 years and a 10/1 ARM 10 years).

- Periodic Changes: The interest rate can fluctuate every year based on the periodic caps.

- Technical terms: An ARM comes with some technical terms. Make sure that the lender gives you the details about:

- Periodic caps: How much can the interest rate increase at each periodic change? Will interest rates over the cap be carried over to the next period? Also, how much can the interest rate change on the first change after the 7 year period.

- Lifetime caps or ceilings: What is the lifetime cap on the loan?

- Floors: Is there a minimum interest rate?

- Index and Margin: What is the base rate for the interest rate at the time of the periodic change and how much is the margin over that rate? How does that compare with today’s rate? Two common indexes are the 1-year T-bill and the 1-Year USD LIBOR rate. Here are some rates for June 2012: the margin is currently 2.25% plus LIBOR for LIBOR ARMS and TBill ARMS are at 2.75% plus TBill .

When looking at different loan options, compare mortgage rates and mortgage fees including origination points, discount points and other lender related fees. In addition, check if there are prepayment penalties, and if so at what time they exist. (Some lenders have prepayment penalties if you pay before the end of the first period. In some cases it applies if you sell or refinance and in other cases only if you refinance).

Compare Mortgage Rates

Compare today’s rates at Bills.com mortgage rate table.

Monthly Payments – Different Scenarios

The 7/1 ARM comes with a lower interest rate than a 30-year FRM. In general, if you are looking for a short-term loan, then a FRM will probably be your preferred loan, especially in a low interest rate environment as in 2011-2012.

In order for you to get a better feel for the difference in payments the table below illustrates different monthly payment possibilities for a $250,000, based on the following information:

| 30-Year FRM | 7/1 ARM (initial and subsequent changes at 2%, ceiling at 7%) | 7/1 ARM (initial change reaches maximum of 7%) | |

|---|---|---|---|

| Initial Interest rate | 3.75% (no change) | 2.75% | 2.75% |

| Monthly Payment First 7 Years | $1,157.59 | $1020.6 (2.75%) | $1020.6 (2.75%) |

| 8th Year | $1,157.59 | $1,243.62 (4.75%) | $1,522.49 (7.00%) |

| 9th Year | $1,157.59 | $1,481.38 (6.75%) | $1,522.49 (7.00%) |

| 10th - 30th Year | $1,157.59 | $1,511.532 (7.00%) | $1,522.49 (7.00%) |

Your monthly payment will be $137.19 less for the first 84 months. However, in the worst-case scenario your payment will increase by $364.90 in the subsequent 23 years.

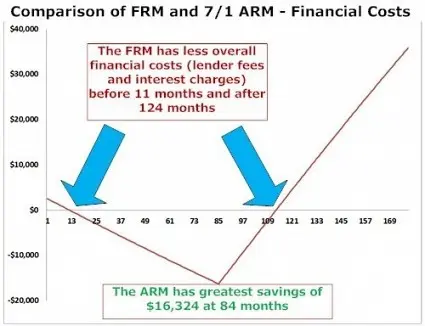

Example #2: Overall Financial Savings: The example below illustrates the nominal financial savings (not including tax and the discounted cost of money) between the following two loans:

- 30-year FRM, 3.5%, 1% lender fee

- 30-year 7/1 ARM, Initial interest rate 2.375%, periodic change (including initial change after 7 years) 2%, lifetime cap (ceiling) 7%., 2% lender fee

If you choose the 7/1 ARM, you will be at a financial loss due to the higher lender fee. However, after 11 months and until 84 months your financial savings will increase, reaching $16,323. It will then gradually decrease until the FRM is the more beneficial loan after 124 months.

Remember, the only sure comparison is until the first interest rate change which in a 7/1 ARM occurs on the 84th payments. The example assumed a constant annual increase of 2% after the initial fixed period. If the lender allowed a larger increase on the first raise, for example up to the 7% ceiling, then your breakeven point would be even lower. On the other hand, interest rates can remain stable or even decrease over the period of the loan, offering you larger gains.

Compare Mortgage Rates

compare frm to arm rates and get a real mortgage quote from bills.com’s mortgage providers.

Choosing an ARM

Before you choose an ARM make sure that the lender explains to you all the technicalities, especially the type of ARM (10/1, 7/1, etc.), the lifetime cap, the periodic caps and the cap on the initial changes. Make sure you understand the worst-case scenario.

An ARM is especially beneficial if your initial interest rate is lower than a comparable fixed rate loan for the same period. (Maybe you can afford an attractive 15-year fixed mortgage rate). A 7/1 ARM (or even 5/1 or 10/1) is beneficial if:

- You are planning on moving and selling the house before the end of the first period (or even a bit longer).

- You have sufficient income and/or assets to cover the higher payment.

However, ARMs carry risks. Some of the cons are:

- You are unable to make higher payments. Some borrowers are tempted to take the ARM (or even an I/O loan) because the beginning payments are affordable hoping that they can later afford the larger payments, or even better the payments will not increase. The failure to make timely payments is expensive and can lead to default and foreclosure.

- You are unable to sell the house, forcing you to stick with the ARM loan and swallow interest rate increases, which make the loan more expensive than the original FRM offered.

- Higher initial lender fees.

In a mortgage market of low interest rates, such as 2011-2012, fixed rate mortgages are popular. This Is especially true for those taking shorter term mortgages, like 15-year FRMs. However, if you understand and can handle the risks, an ARM, including the 10 year ARM, is a good option to explore.