Learn How A Reverse Mortgage Works

- A reverse mortgage is different than a purchase, refinance, or home equity mortgage.

- You choose the way you want to receive money.

- You don't have monthly mortgage payments, but must make property tax and homeowner insurance payments.

Does a Reverse Mortgage Work for You?

We are all familiar with different types of loans, auto loans, mortgage loans, credit card debt. They have payment schedules (or at least minimum payments) and a due date.

Well, reverse mortgages don’t work like most mortgage loans. Sure, a reverse mortgage is a loan, but you don’t make monthly payments. In fact, you aren’t even personally responsible to pay it back.

A reverse mortgage is a special type of mortgage loan available to borrowers over the age of 62 who have equity in their home. Once the last surviving borrower moves out of the house or passes away the loan comes due. A reverse mortgage loan works in different ways than most mortgages. It is a complicated financial tool. You need to consider how a reverse mortgage fits into your overall financial retirement plan.

Quick Tip #1

Learn how a reverse mortgage works and Get a reverse mortgage quote from a pre-screened Bills.com reverse mortgage provider.

Reverse Mortgage: How it Works

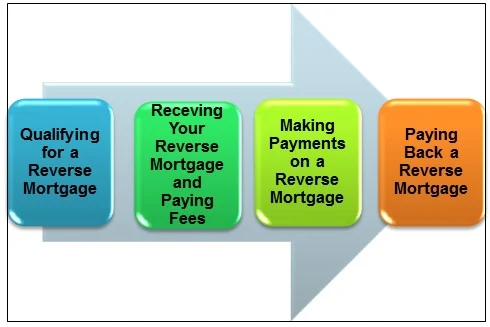

In order to help you learn whether a reverse mortgage is appropriate consider how a reverse mortgage works. This article will help you understand how a reverse mortgage works and how it is different from other types of loans across these four points:

Qualify for a Reverse Mortgage

A reverse mortgage works much differently than a regular mortgage loan. A home mortgage loan (purchase or refinance) requires a large number of documents and a complicated underwriting process whereby the lender gathers, checks and verifies your income, debts, assets, and property.

Qualifying for a reverse mortgage is much simpler, focusing on these elements:

- Age: A borrower must be over the age of 62.

- Property Value and Equity: The amount of equity you have in your house (the value of the house less any mortgages or liens). Note: The property must be your primary residence.

- Minimal financial check: The borrower must show ability to pay property tax, homeowner insurance, and basic maintenance expenses.

Receiving Your Reverse Mortgage Loan

A reverse mortgage, as its name suggest, is very different from a regular mortgage loan or home equity loan. These are the different methods how you can receive your reverse mortgage. You can choose to receive your reverse mortgage in one of the following manners (or a combination of them):

- Lump Sum: You can receive all the proceeds in one lump sum.

- Monthly Payment for a specified period or for the entire period you stay in your home.

- Line of Credit: You can draw funds, as you need them, up to the amount of your line of credit. The line of credit is adjusted based on the interest rate (which is variable) and the amount you take. (It is possible that the amount will increase).

Tip: A fixed rate mortgage is available only in a lump sum. However, this is not always the optimal manner to take a reverse mortgage. Make sure you understand how the different ways you can take your reverse mortgage fit into your overall retirement financial plan.

Update

Beginning on April 1, 2013 the fixed rate HECM will be available only through the HECM saver option. For more information read the Bills.com article about the HUD backed HECM (Home Equity Conversion Mortgage).

Reverse Mortgages have a number of fees, which are generally deducted from the loan proceeds. Here are some of the major types of fees:

- Lender Origination Fee: This fee is a percentage of your loan that goes to the lender.

- Mortgage Insurance Premium: This protects your ability to drawdown the full amount of money, no matter what happens to the lender. It also protects the lender in the case that the home value is less than the loan.

- Loan Servicing Fee: The lender deducts from your loan a sum to cover a monthly service charge over the projected life of the loan.

- Counseling Fee: All HUD backed reverse mortgages require a counseling service, which costs about $125.

- Various mortgage fees: (Check if they are paid out of pocket or from loan proceeds). This includes appraisal, document preparation, title insurance, escrow fee, survey fee, and other special third party services).

Making Payments and Fees

A reverse mortgage does not require any monthly payments. Your interest accumulates (based on the amount you borrow) and is added to the principal. One important point you need to make sure that you understand and properly prepare for is that you have to continue to maintain these payments:

- Property tax

- Homeowner Insurance

- Other required homeowner payments

- Basic Maintenance fees.

Remember, if you cannot maintain those payments, then the lender may have the right to demand immediate payment of your reverse mortgage loan. Choosing the type of reverse mortgage (lump sum, monthly payment, line of credit, or combination) is an important step. Make sure that you work out your future financial needs to ensure that you can maintain all those payments.

Paying Back a Reverse Mortgage

A reverse mortgage helps the borrower stay in their home, with no monthly mortgage payments. You do not need to pay the loan back as long as you meet these criteria:

- You maintain your monthly-required housing payments including property tax, homeowner insurance and basic maintenance fees.

- You remain in the home. If you leave for an extended period, whether to a nursing home or a different residence, then you may be required to pay back the reverse mortgage loan.

If you sell the property, then you need to pay the loan back.

However, the reverse mortgage loan works in such a way that the surviving spouse or the heirs may need to take care of the reverse mortgage. This is a tricky part of the reverse mortgage and make sure that your lender and your counselor explain the different scenarios to you. There are many examples of spouses begin left off the loan (some are even taken off title to allow for a larger loan or because they are too young to qualify) and then having trouble when the spouse passes away.

Surviving spouse: If the surviving spouse was a borrower, then they have the right to stay in the house as long as they meet the two basic loan requirements stated above. However, if the surviving spouse is not on the loan (because they were not on the title or they were too young to qualify for a reverse mortgage), then it is very important to clarify the rights and obligations of the non-borrowing spouse.

Heirs: Heirs do not need to pay back the loan from their own personal funds. The loan is paid back from the proceeds of the sale of the property. If there are insufficient funds, then the loan is cancelled and the estate has no further obligations. If the property is worth less than the balance of the loan, then the loan is cancelled upon the sale of the property. Alternatively the heirs can purchase the property (and pay back the loan) based on the lower of the loan balance or 95% of the appraised value of the home.

Reverse Mortgage: Making it Work for You

A reverse mortgage is a complex financial tool that helps many people stay in their homes and manage their budgets. Reverse mortgages work much differently than a regular mortgage. Here are three main ways that reverse mortgages differ:

- You decide on how you want to take the money, either a lump sum, set monthly payments, a line of credit, or a combination of those methods.

- You don’t have any monthly mortgage payment. (However, make sure that you can pay your housing expenses)

- You have higher upfront fees, which are deducted from your loan.

How can you make a reverse mortgage work for you? Here are the steps you should take to make sure that the reverse mortgage is the right loan for you:

- Prepare your budget and understand your long-term retirement needs.

- Decide how long you want to stay in the house?

- Learn about the pros and cons of a reverse mortgage.

- Take the time to learn about a reverse mortgage and you have all your questions answered.

Quick Tip #2

Prepare yourself and Get a reverse mortgage quote from a pre-screened Bills.com reverse mortgage provider.