- The FHA showed negative capital at the end of 2012.

- The FHA is going to raise mortgage insurance premiums to improve revenue.

- The FHA may raise minimum credit score requirements and lower its loan limits.

Avoiding FHA Bailout - New Proposals and Loan Requirements

Update - December 18, 2012

Following Sec. Donovan's testimony to the Senate Banking Committee on December 18th, Carol Galante, acting commissioner of the Federal Housing Agency, sent a letter (PDF) to Sen. Bob Corker (R-Tenn) informing him of the FHA's intent to make changes in their mortgage programs including:

- Minimum Credit Scores: increase the debt to income ratio (DTI) for credit scores lower than 620 and require manual underwritten loans only, with documentation of compensating factors such as higher down payment or large reserves.

- Changes in Reverse Mortgage Rules: Place a moratorium on the Full Draw HECM Reverse Mortgage product as well as other.

- Scale Back of FHA Market Share: The FHA offers higher loan limits than for conforming loans. Galante indicated that the FHA would offer stricter terms for the larger loans (over $625,000), to "drive business to the private market".

- Increase Mortgage premiums: Galante indicated that the FHA will increase the mortgage insurance premium for larger loans to the maximum, currently 1.55% (or 155 bps).

- Increase down payment requirements: The letter committed the FHA to change their maximum loan to value ratio for larger loans. Instead of the current 3.5% down payment, borrowers will need to put in at least 5%.

4. Tighten loan requirements after foreclosure: FHA has more lenient guidelines than Fannie Mae or Freddie Mac regarding getting a loan after a foreclosure. Today a borrower can get a FHA-insured loan three years after a foreclosure. However, Galante noted that the FHA provided the leniency only for those who "re-established good good and qualify for an FHA loan...". The FHA in no way means for this to be an automatic condition and will step up its enforcement.

Galante promised to implement these changes by January 31, 2013. Bills.com will continue to update you about these and other changes in the FHA mortgage programs.

The FHA continues to struggle with losses, especially those relating to their single-family mortgage loan programs. According to an independent audit, the FHA is running a negative capital reserve of $16.3 billion. If the FHA does not take aggressive corrective actions, it may need to draw upon treasury funds (a bailout by taxpayers) in order to meet their financial obligations.

How the FHA's Financial Problems Affect You

Due to the seriousness of their problem, the FHA is planning to make a number of changes in their mortgage programs, including:

- Raising mortgage insurance premiums

- Raising minimum credit score

- Lowering loan limits

- Terminating the cancellation of Mortgage Insurance Premiums

Secretary of HUD (Housing and Urban Development), Shaun Donovan, presented to the Sen. Banking Committee testimony, on December 6, 2012, regarding the FHA’s financial position and plans for the upcoming year. The FHA has yet to announce firm changes in their program, however HUD Secretary Shaun Donovan indicated that some of these changes will commence in 2013.

Sec. Donovan indicated in his testimony that he is concerned about the possibility of a bailout; however, the FHA is planning on increasing its revenue and cutting its loss through new loan requirements and other administrative actions. He hopes that the FHA can avoid tapping into the treasury. A strong housing market recovers will help restore the FHA's balance sheet (due to appreciation of housing prices). Sec. Donovan is taking steps to balance between helping weaker sectors of the economy receive mortgage loans and purchase homes without hurting the FHA's precarious financial situation and at the same time ensure that the housing market recovers.

Quick Tip

Looking for a mortgage? Purchase? Refinance? Take advantage of today's historically low mortgage rates and get a mortgage quote from a Bills.com mortgage provider for an FHA loan or a conventional loan.

The FHA Single Family Mortgage Program

The FHA mortgage program is an important loan program, especially for borrowers with either a credit scores and/or low down-payment that would prevent them from qualifying for a conventional loan. Although FHA loans have high upfront mortgage fees and high monthly mortgage insurance premiums, they are an important source of funds for mortgage borrowers, especially first-time homebuyers.

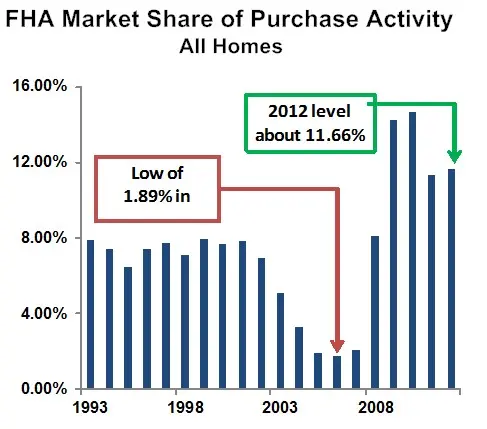

The FHA's market share of purchase loans dropped during the 2005-2008 period to about 2% for all home loans. Since then it has increased, reaching about a 12% market share. The chart below shows the market share for all home purchase loans since 1993 through the first 7 months of 2012.

FHA: Steps to Avoid a Bailout — A Look Back at 2012

Here are some of the steps that the FHA has taken to increase its revenues or cut its losses:

Increased supervision over lender network: This includes better supervision over lenders' compliance with underwriting and service requirements.

- The National Mortgage Settlement, which targeted big lenders for their poor foreclosure activities, brought in $1 billion of income.

Increased down-payment requirements: The FHA increased credit score requirements to 580 (from 500) for the 3.5% down-payment requirement. They also eliminated seller funded down-payment assistance programs

- Based on the 2012 Actuarial report the 2005-2008 loans contributed about 1/3 of the total losses. The loans with credit score under 580 and/or seller-funded down-payment assistance accounted for more than 44% of these losses.

Increased Mortgage Insurance Premiums (MIP): Since 2009, the FHA has raised the MIP four times, including once in 2012. The current standard rate is an upfront fee of 1.75% and a monthly fee of 1.15 or 1.25%.

- The FHA has increased revenue by more than $10 billion since 2009. Their policy has been to tread lightly and provide a counter-balance to the housing crisis and keeping credit available, especially to first-time buyers and weaker sectors.

Asset Management: The FHA is also improving their portfolio by selling non-performing loans and improving the sale and management of foreclosed properties.

- The FHA has reduced the time in inventory by 45% and decreased the gap between appraised values and sales prices by 62%

FHA: A look Ahead to 2013 — New FHA Loan Requirements and Actions

In order to bolster their financial position the FHA is considering the following steps:

- Change MIP cancellation policy

- Increase minimum credit score

- Lower Loan Limits

MIP Policy — Increase Fees and Change Cancellation Policy

Raise MIP Fees: The FHA is already planning on raising the mortgage insurance premiums in 2013 at least another 10 basis points, or 0.1%. That translates to another $200 per year for a $200,000 loan.

Cancel Termination Policy: Currently the FHA provides a lifetime guarantee for loans it books; however, in general, the borrower only pays premiums until the loan reaches a 78% loan to value ratio (LTV), based on the original value of the house and the original payment schedule. In contrast, Private Mortgage Insurance (PMI) has limited coverage (not 100% of the loan, but up to 30%. PMI has an automatic termination clause, generally 78%. Once terminated the borrower no longer pays for the insurance and the lender is no longer covered for potential losses.

Because of the drop in housing values, the FHA is facing increasing amounts of loans in which the borrower no longer pays for insurance, but the FHA still guarantees 100% of the loan. Sec. Donovan indicated in his remarks to the Senate Banking Committee on December 6, 2012, that there will be an increase of 10 basis points, or 0.1% on FHA loans, beginning in 2013.

Tighten Underwriting Policies

A major criticism of the FHA is that it is carrying a loss due to its very lenient loan underwriting process. This included the following elements:

Increase the minimum credit score: The FHA’s current policy of a minimum credit score of 580 (for loans with 3.5% down-payment) is not in line with other mortgage programs and lenders policies. The general rule is a 620 credit score.

- Sec. Donovan did not commit to any firm number, however indicated that there is a need to create new underwriting rules.

Lower Loan Limits: The FHA loan limits are significantly higher than Fannie Mae and Freddie Mac conforming loan limits. Currently, the standard conforming loan limits are $625,500, while the FHA’s loan limits are $729,000.

- Sec. Donovan came out in favor of lowering loan limits, however he indicated that this will require Congressional action. According to an FHA announcement of December 12, 2012, the 2013 maximum loan limits are not changing.

Post-Foreclosure Requirements: The FHA has less stringent past-foreclosure requirements, allowing a borrower who experienced a foreclosure to qualify for an FHA loan after a 3-year waiting period, versus Fannie Mae and Freddie Mac’s 4-7 year waiting period.

- Once again, while there is pressure to establish stricter credit requirements, the FHA is not committing itself to these changes. Sec. Donovan believes that there needs to be opportunities for those hit by the economic crisis, including borrowers who may have had a foreclosure.

FHA Loans: New Loan Requirements and Fees?

The FHA is suffering huge losses, mainly due to poor loans it booked during the 2005-2008 period. The huge downturn in housing prices added to their losses and created a potential for a treasury bailout.

During 2012, the FHA has already taken steps to improve its financial position, including improving the management of their portfolio and increasing prices to the consumer. The FHA, being an important player in today’s mortgage market, is trying to balance between profitability and supply.

FHA loans are an important source of loans for borrowers with lower credit scores and/or lower down payments. This is especially true for first-time homebuyers. Upcoming changes, including the increase in MIP will certainly change the market.

Bills.com will continue to provide updated information about FHA and other mortgage loan requirements.

Quick Tip

Shopping for a mortgage? Take advantage of today's historically low mortgage rates and get a mortgage quote from a Bills.com mortgage provider.