Lexington Law Reviews - Will Credit Repair Work For You?

- Understand how credit repair works and if the service can help you.

- Review Lexington Law's methods and standing.

- Read hundreds of reviews and comments from readers about their experience with the Lexington Law credit repair process.

- Start your FREE debt assessment

I recently hired Lexington Law Firm to help fix my credit and do credit repair. Are they good? Can you share Lexington credit repair reviews?

I recently hired Lexington Law Firm to help fix my credit and do credit repair for me. Are they good? I have seen a few complaints and even allegations that "Lexington Law scam" concerns are out there on the internet. For my case, I have 10 negative items on each report for Experian, Equifax, and TransUnion. I thought they would challenge all of my negative items on all reports all at once. However they told me that they intentionally limit the number of items to protect their clients. They said the Fair Credit Reporting Act allows the bureaus to refuse to reinvestigate any challenges that they consider frivolous. One factor they use in determining a frivolous challenge is when a consumer challenges too many things at one time. They also said they found that limiting the number of items they challenged will avoid their clients challenges from being labeled as frivolous. Are they feeding me a bunch of bull or does this sound right to you? Can you do a Lexington Law review?

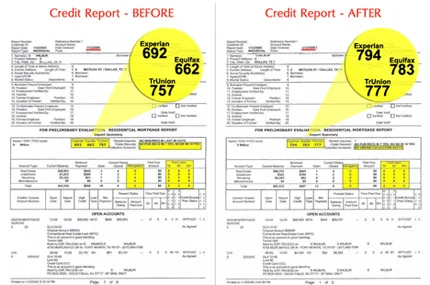

Since first writing our review of Lexington Law and evaluating their services in particular, and credit repair more generally, we received hundreds of comments from clients and consumers.

There is nothing any credit repair organization can legally do for you — including removing inaccurate credit information — which you can’t do for yourself, for free. However, you may decide it is worth paying an organization to take care of these matters for you. The fees can be substantial, ranging from hundreds to thousands of dollars.

The Credit Repair Organizations Act (CROA), a federal law, prohibits credit repair organizations from taking consumers’ money until they complete the services promised. It also requires such firms to provide consumers with a written contract stating all the services to be provided and the terms and conditions of payment. Consumers have three days to withdraw from the contract.

Credit repair is not effective for current, unpaid debts. Even if current debts fall off a credit report, they will reappear at the next reporting period. You need to get out of debt before seeking to remove a debt from your credit report.

Lexington Law Credit Repair Reviews

The activities of credit repair companies are constrained by the Fair Credit Reporting Act (FCRA) and the Credit Repair Organizations Act (CROA). Bills.com is not in a position to be able to verify whether Lexington Law Firm complies with these and other federal and state laws and regulations. Educate yourself about credit repair and the CROA before proceeding.

Under the FCRA, if a consumer credit reporting agency receives what it (in its opinion) deems as a frivolous challenge, then that credit reporting agency can ignore the request. Credit repair companies cannot guarantee success because creditors have such a large influence on what appears in a credit report. Also, the credit reporting agencies deal with so much data, it is a mix of art and science for a person or credit repair company to change or delete a listing on a credit report.

Lexington Law has been in business for quite some time. Any company with many clients over a number of years, such as Lexington Law, will generate complaints on consumer Web sites where readers claim the company is a scam. Of course, each consumer needs to do their own homework.

Lexington Law Firm Will Not Erase Your Debt

Lexington Law Firm cannot get you out of debt. Contact one of Bills.com’s pre-screened debt providers for a no-cost, no-hassle debt relief quote.

Letter of Deletion

Use a letter of deletion to request the removal of inaccurate information from a credit report. A sample letter of deletion is below, and we include instructions for how to submit it online at no cost.

No one can remove accurate and timely negative information from a credit report legally. The law allows you to ask for an investigation of information in your file that you dispute as inaccurate or incomplete. There is no charge for doing this on your own. If you paid the accounts in full and as agreed, then you can try to get them removed.

Following up with the credit bureaus might be a time-consuming proposition, depending on how many items you want to be removed. To get these items removed from your credit report you have two options:

1. Pay For The Services of a Credit Repair Firm

Lexington Law Firm is one of many a credit repair companies. Be careful about the firm that you choose and make sure that it is a reputable firm. Check with the Better Business Bureau to learn about the performance of a particular company. Do some research on the firm you will eventually do business with. By law, credit repair companies must give you a copy of the “Consumer Credit File Rights Under State and Federal Law” before you sign a contract. They also must give you a written contract that spells out your rights and obligations. Read these documents before you sign. The law contains specific protections for you. For example, a credit repair company may not:

- Make false claims about their services

- Charge you until they have completed the promised services

- Perform any services until they have your signature on a written contract and have completed a three-day waiting period.

- Suggest you mislead credit reporting agencies about your accounts or alter your identity to change your credit history

Your contract must specify:

- The payment terms for services, including their total cost

- A detailed description of the services to be performed

- How long it will take to achieve the results

- Any guarantees offered

- The company’s name and business address

2. Do It Yourself

Bills.com offers a debt self-help center that can help you solve your debt problems on your own for free. Step one is to obtain a copies of your credit reports from the three largest consumer credit reporting agencies. Go to AnnualCreditReport.com for no-cost, no-gimmick copies of your credit reports. Alternatively, call (877) 322-8228, or write to Annual Credit Report Request Service, P.O. Box 105281, Atlanta, GA 30348-5281. You may order your reports from all three nationwide consumer reporting companies at the same time, or you can order your report from each of the companies one at a time.

Check your reports for the action items. The three biggest bureaus allow consumers to dispute items online, but in most cases you will need a copy of the respective report and other information to do so. Once you are ready, contact the bureaus reporting the incorrect information:

| Equifax | Experian | TransUnion |

|---|---|---|

| 800-685-1111 | 888-397-3742 | 800-916-8800 |

| Equifax.com | Experian.com | TransUnion.com |

| File a credit dispute online at Equifax | File a credit dispute online at Experian | File a credit dispute online at TransUnion |

Dispute errors with the consumer credit reporting agencies directly. Source: Bills.com

Sample Letter of Deletion

Tell the consumer reporting company, in writing, what information you think is inaccurate. Include copies (not originals) of documents that support your position. In addition to providing your complete name and address, your letter should clearly identify each item in your report you dispute, state the facts and explain why you dispute the information, and request that it be removed or corrected. You may want to enclose a copy of your report with the items in question circled.

Your letter may look something like the following:

| FTC Sample Letter of Deletion |

|---|

| Date Your Name Your Address Your City, State, Zip Code Complaint Department Name of Company Address City, State, Zip Code Dear Sir or Madam: I am writing to dispute the following information in my file. The items I dispute also are encircled on the attached copy of the report I received. This item (identify item(s) disputed by name of source, such as creditors or tax court, and identify type of item, such as credit account, judgment, etc.) is (inaccurate or incomplete) because (describe what is inaccurate or incomplete and why). I am requesting that the item be deleted (or request another specific change) to correct the information. Enclosed are copies of (use this sentence if applicable and describe any enclosed documentation, such as payment records, court documents) supporting my position. Please investigate this (these) matter(s) and (delete or correct) the disputed item(s) as soon as possible. Sincerely, Your name Enclosures: (List what you are enclosing) |

Sample Letter of Deletion. Source: FTC

Conclusion

Credit repair will not erase or cancel unpaid debt from your credit reports. Clear your debts before trying credit repair.

Follow the steps above to dispute incorrect information on your credit reports. If the provider reports the item to a consumer reporting company, it must include a notice of your dispute. If you are correct — that is, if the information is found to be inaccurate — the information provider may not report it again.

Some Web sites provide kits for as little as $13.95 that contain letter templates and tips to help you repair your credit yourself. You can learn more about credit, credit scoring, and credit repair at Bills.com.

Generally we do not believe that firms like Lexington Law, Ovation Law, and other credit repair industry leaders are scams, even though they do have lots of complaints about them on consumer-complaint Web sites. Be sure to evaluate each company’s complaint volume against the size of its overall client base. Do your homework to ensure the monthly fee seems reasonable to you for the services promised. Many of the unhappy people who comment below failed to do their homework, and as a result were disappointed.

I hope this information helps you Find. Learn & Save.

Best,

Bill

Free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Actual client of Freedom Debt Relief. Client’s endorsement is a paid testimonial. Individual results are not typical and will vary.

10 Comments

I love lexington law, I really appreciate all of your hard work, I had 14 bad remarks on my credit with in 60 days 8 was removed out of 14, I love the fact that if I don't understand they brake it down so I can. Now I'm not saying this is gonna happen for everyone but it never hurts to give it a try. And also understand that the time we put is messing our credit up it may take half that time to repair it.

I used lexington Law's top premium service ( paying $129 a month) They did next to nothing for me. they would challenge the Credit bureaus and when I would get a response via a form letter, they would never do ANY followups at all. In fact, when I called them they said I needed to do all the following up. When I asked what I pay them for and what is included in my "premium service" plan if I have to all the work to repair my credit, and their response was we will not do any further investigation with any creditors to validate how they checked their information. This is a scam folks, they siphon your money away while dragging their feet on any items that you may need worked on. and will do little to no additional work to have form letter responses investigated any further. They will say to you that even though you PAY them to do this work, that it is YOUR responsibility. don't waste your money on these people, they are a fraud.

Quick advice. Pay attention to tho comments about fast credit experts being scams and fakes.

Credit repair requires some tips, creativity, and knowledge of the causes, solutions, and credit systems. It is more art than science. Knowing about tips and Repairing your credit score, either on your own or with a repair firm, is no guarantee of a clean record.

Varinder, thank you for your input. I would advise against spending money with a credit repair firm to remove any accurately reported derogatory information.

The information in the article correctly reflects the CROA requirements. Here are two links to with more information: FTC US Code of LAW, which clearly states, among other points:

§1679d. Credit repair organizations contracts (a) Written contracts required No services may be provided by any credit repair organization for any consumer— (1) unless a written and dated contract (for the purchase of such services) which meets the requirements of subsection (b) has been signed by the consumer; or (2) before the end of the 3-business-day period beginning on the date the contract is signed. (b) Terms and conditions of contract No contract referred to in subsection (a) meets the requirements of this subsection unless such contract includes (in writing)— (1) the terms and conditions of payment, including the total amount of all payments to be made by the consumer to the credit repair organization or to any other person; (2) a full and detailed description of the services to be performed by the credit repair organization for the consumer, including— (A) all guarantees of performance; and (B) an estimate of— (i) the date by which the performance of the services (to be performed by the credit repair organization or any other person) will be complete; or (ii) the length of the period necessary to perform such services;

I used Lexington Law for 3 months and they did nothing for my credit. They sent letters to the three credit bureaus but that was it. They did nothing I couldn't have done myself. I paid $129 for the first month and then, after calling and requesting it, I paid $54 per month for the next 2 months and then I canceled. I worked with a credit repair company in 2014 (I can't remember the name, it wasn't Lexington Law) and they were able to improve my credit so that I was able to buy my house. Bottom line: do NOT use Lexington Law! There are actual companies that work but they are not among them!