- Home mortgage loans are a complex financial product.

- The CFPB proposed new forms to replace the GFE and TIL forms.

- The comparison tools on the Loan Estimate Form are unclear.

Mortgage Disclosure: Getting a Mortgage Loan

Editor's Note

The CFPB announced on December 13, 2012 proposals to allow testing on new disclosure statements, including the mortgage disclosure statements. The testing will be for a limited time by companies that meet the CFPB's requirements. We all know that the current forms are confusing and duplicative. This article explains the CFPB's proposed Loan Estimate form.

Getting correct, timely and useful information is necessary for anyone looking for a home mortgage loan. Mortgages are a complex and complicated financial transaction involving large sums of money. Anyone who has ever shopped for a mortgage loan realizes that it takes time and preparation to get a loan.

The way mortgage lenders and brokers disclose information makes a big difference in how you understand the terms, risks, and costs of your mortgage offers. The Consumer Financial Protection Bureau (CFPB) is near the end of a long process to get you better information and more transparent mortgage disclosure forms.

To help you find the best mortgage loan for your financial situation, learn about proposed mortgage disclosure rules, including:

- CFPB: Mortgage Disclosure — Improving the System

- CFPB: The Mortgage Disclosure Process

- General Characteristics of a Mortgage Loan

- Mortgage Application and The New Estimated Loan Disclosure

CFPB: Mortgage Disclosure — Improving the System

The key to making a sound decision about your mortgage is:

- Getting timely and correct information

- Understanding your costs and risks

- Comparing deals between lenders and from one lender over time.

The 2008 housing and mortgage crisis left many borrowers struggling to pay back their loan. Some borrowers are underwater (an estimated 11 million) and many are seeking alternatives to foreclosure. Unfortunately, lax underwriting standards by lenders coupled with borrowers who did not fully understand the implications of their loans made for a market with many unaffordable loans.

Following the financial crisis, Congress passed the Dodd-Frank Act, to tighten up the laws and regulations regarding the financial industry. The CFPB was created to regulate the financial sector. Among their top priorities is the mortgage market. This article discusses mortgage disclosures when you are shopping for a loan.

We welcome your comments about problems with the mortgage disclosure forms and/or suggestions for improvements.

Editors Note

Repairing the mortgage market is a top priority for the newly created CFPB. This article deals with mortgage disclosure and the initial stage of getting a mortgage — the application stage and the Loan Estimate disclosure form. The CFPB is currently working on other mortgage topics, including the Closing Disclosure Form, Ability to Repay Mortgage Rule, Loan Officer Compensation Rule.

CFPB: The Mortgage Disclosure Process

The ultimate goal of the CFPB is to ensure that you will be able to understand the terms and risks of your mortgage loan. The CFPB is drafting new rules to ensure that the consumer receives clear forms so that you can easily compare:

- Offers from different lenders

- An offer from one lender between application time and closing time. This includes standardizing the APR calculation and the amount of changes that can occur between application time and closing time.

The new rules are an attempt to create a more efficient system. Today there are two regulations, Regulation X, part of the Real Estate Settlement Procedures Act (RESPA), and Regulation Z, issued by the Board of Governors of the Federal Reserve System. Different mortgage disclosure forms were created and the CFPB is proposing to combine them into two forms as follows:

| Stage | Current Forms | Proposed Form |

|---|---|---|

| Application | Regulation X: Good Faith Estimate (GFE) Regulation Z: Truth in Lending (TIL) | Combined Loan Estimate Form |

| Closing | Regulation X: HUD-1 Closing Form Regulation Z: Revised TIL Closing Form | Combined Closing Disclosure Form |

Scope: The new CFPB mortgage disclosure will cover most home mortgage loans, but the proposed rule does not cover home-equity lines of credit, reverse mortgage. The CFPB proposal includes a few exceptions as follows, “The proposed rule does not apply to home-equity lines of credit, reverse mortgages or mortgages secured by a mobile home or by a dwelling that is not attached to land. The proposed rule also does not apply to loans made by a creditor who makes five or fewer mortgages in a year.”

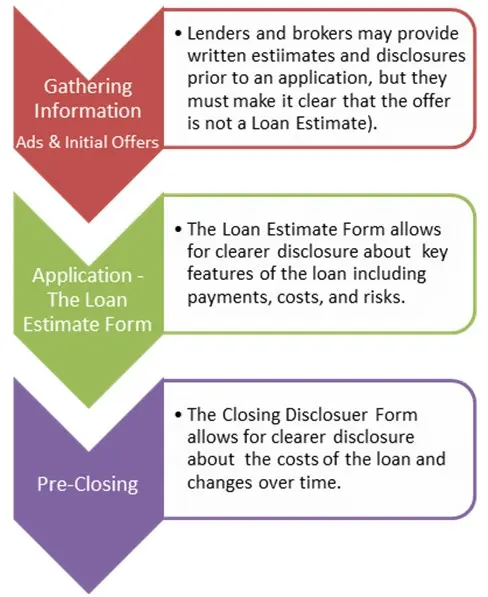

The three main stages in the pre-closing mortgage process are:

- Gathering Information — Advertisements and Initial Offers: Advertisements only require general disclosure information. Also, initial offers (pre-application) do not require a mortgage disclosure form. However, the lender must make a disclaimer that the offer is not a Loan Estimate Form. At this stage, you do not need to divulge your full information.

- Making an Application: Once you submit an application, the lender must provide to you, within three business days, a Loan Estimate Form. According to the CFPB’s current proposal, as published in the Federal Registry, the CFPB defines an application, based on a limited Regulation X definition, including

“the six pieces of information specified in proposed § 1026.2(a)(3)(ii), which are

- “the consumer’s name,

- “income, and

- “social security number to obtain a credit report,

- “as well as the property address,

- “an estimate of the value of the property,

- “and the mortgage loan amount sought.”

- Pre-closing: The pre-closing disclosure form is designed to make it easier to track the changes made between the time you receive the Loan Estimate form and closing. The lender is required to send out the form three business days before closing.

Here is a brief description of what to expect during your mortgage shopping experience, before you close the loan:

General Characteristics of a Mortgage Loan

Before shopping for a mortgage loan, make sure that you prepare yourself by understanding the basics about mortgage terms and qualifying for a mortgage. While this is not a comprehensive list, here are some of the critical factors that distinguish one mortgage loan from another (besides the service that the lender or broker offers to you), here are some of the ways you can look at differences between loan offers:

| Characteristic of Loan | Explanation |

|---|---|

| Purpose of Loan | The major types of home mortgage loans are purchase, refinance, and cash-out refinance and home equity loans. |

| Length of Loan | Mortgage loans are offered up to 40 years, although the most common are 30-year and 15-year loans. |

| Interest Rate | Fixed Rate Mortgages (FRM) or Adjustable Rate Mortgages (ARM) |

| Payment Schedule | A FRM with equal payment monthly payments are the most common. However, ARMs have changes in the payment schedule due to fluctuations in the interest rate. There are also loans with interest only payments, balloon payments, and various combinations. |

| Closing Costs | Loans have various costs including lender fees, third-party fees, prepaid and escrow fees. |

| Misc. | Is there a prepayment fine? Do anti-deficiency laws apply? |

Check out Mortgage Rates

To learn about today’s mortgage rates, see Bills.com mortgage rate table.

Mortgage Application and the New Estimated Loan Disclosure

The proposed Loan Estimate mortgage disclosure form is a three-page condensation of the current Good Faith Estimate and Truth-in-Lending forms. Here are links to a PDF file of the proposed Loan Estimate form (PDF) and a Loan Estimate form for a ARM loan (PDF).

Here is a brief summary of the Loan Estimate form:

General Information and payments

This section includes information about the borrower, the purpose of the loans, the type of loan (Conventional, FHA, VA or other), and basic information about the property. It also includes information about a rate lock, which is especially important when mortgage rates are changing.

Loan terms include the length of the loan, interest rate, mortgage payments including principal and interest. The lender must indicate if there are any special conditions such as a balloon payment, or prepayment penalty. Pay special attention to those terms.

This section also includes your projected payments, including principal, interest, mortgage insurance, and estimated escrow payments (and mark if required) of property tax and homeowner’s insurance.

Closing Cost Details

Whenever you shop for a mortgage, you must consider the total cost of the mortgage, including mortgage rates and mortgage fees. However, remember that some of the costs of the loan are not actual financial costs, rather are auxiliary costs of taking a mortgage loan. You will need to know the different fees in order to determine:

- The amount of cash you need to bring to the closing.

- The actual cost of your loan, which will be discussed below in the additional information section.

Loan Costs and Fees

The second page of the Loan Estimate form includes a listing of different types of fees and costs. The CFPB divides the fees into these categories:

- Loan Costs:

- Lender Fees such as points, application fees and underwriting fees.

- Third-party fees you cannot shop for including appraisal report, credit report, flood determination, flood monitoring, tax monitoring and tax status research).

- Third-party services you can shop for including pest inspection, survey fee, and various title fees.

- Other Costs: This includes taxes, government fees (transfer tax and recording fee), prepaid costs (homeowner insurance, mortgage insurance premium, prepaid interest, and property taxes), and other optional services such as title-owner’s title policy.

- Calculations: The Loan Estimate Form provides a calculation of total closing costs, your downpayment, your deposit, and an estimate of the amount of cash you need for closing.

Additional Information

The third page of the CFPB’s Loan Estimate Form includes information to help you understand the financial cost of the loan and other considerations including:

Comparison of loan offers: Unfortunately, for the consumer, comparing loan offers is a difficult process due to a number of factors including, comparing different types of products (FRM vs. ARM), different sets of costs, and different time horizons that borrowers hold on to their loans. The Loan Estimate form includes three tools: APR or Annual Percentage Rate, 5-year Comparison (how much interest and fees you pay after 5 years), and a TIP or Total Interest Percentage (which shows how much interest you pay as a percentage of your loan).

Learn about Comparing Mortgages and APR

For more information about loans, comparison read the Bills.com article about APR and mortgages.

Other important points in the form relate to the need for an appraisal report, loan assumption rights, homeowner insurance requirements, late payment charges, refinancing rights, and notification about possible servicing.

New Mortgage Disclosure Forms — A Step Forward?

The new proposed mortgage disclosure forms are a step forward to creating a more transparent mortgage market and make it easier for you to compare information and offers. Especially helpful is the section that deals with the different types of costs. Less helpful are there tools to help evaluate the offers. It is not clear yet how the ARP will be calculated, and it will certainly not be able to take into account different possible periods that you may hold on to the loan.

However, the current Good Faith Estimate and Truth in Lending forms provide much of the information to be found in the new Loan Estimate mortgage disclosure form. Due to the complexity of a mortgage transaction, no one form is going to be able to make the transaction clear. Make sure that you use Bills.com to understand mortgage terms and find the mortgage loan best suited to your situation .

Get a Mortgage Quote Now

Shop around and get a mortgage quote from a bills.com mortgage provider.