Can a Teacher Making $58K Qualify for Chapter 7 Bankruptcy?

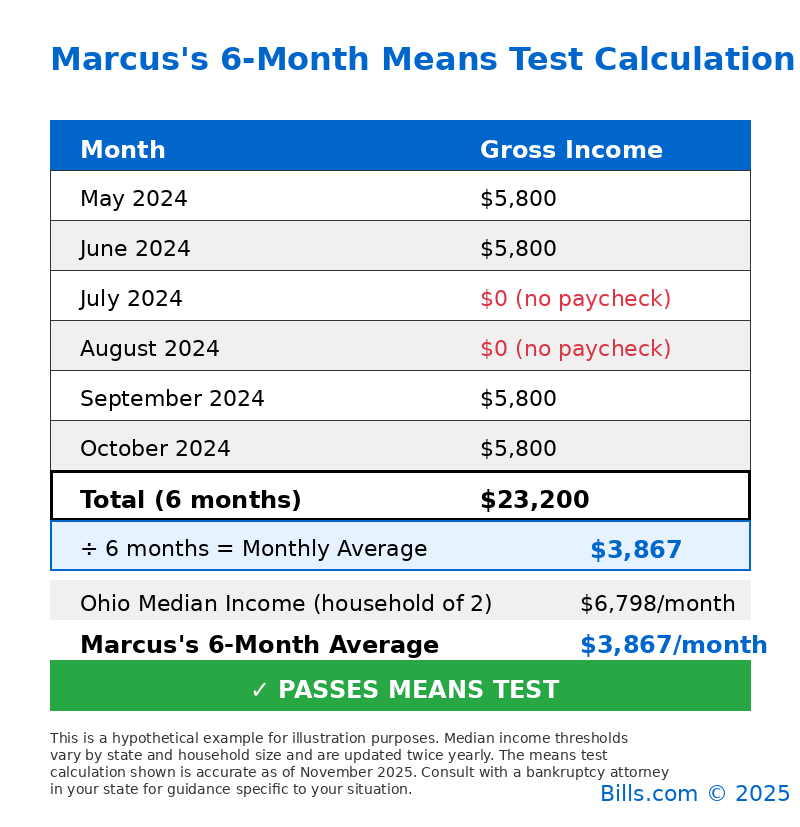

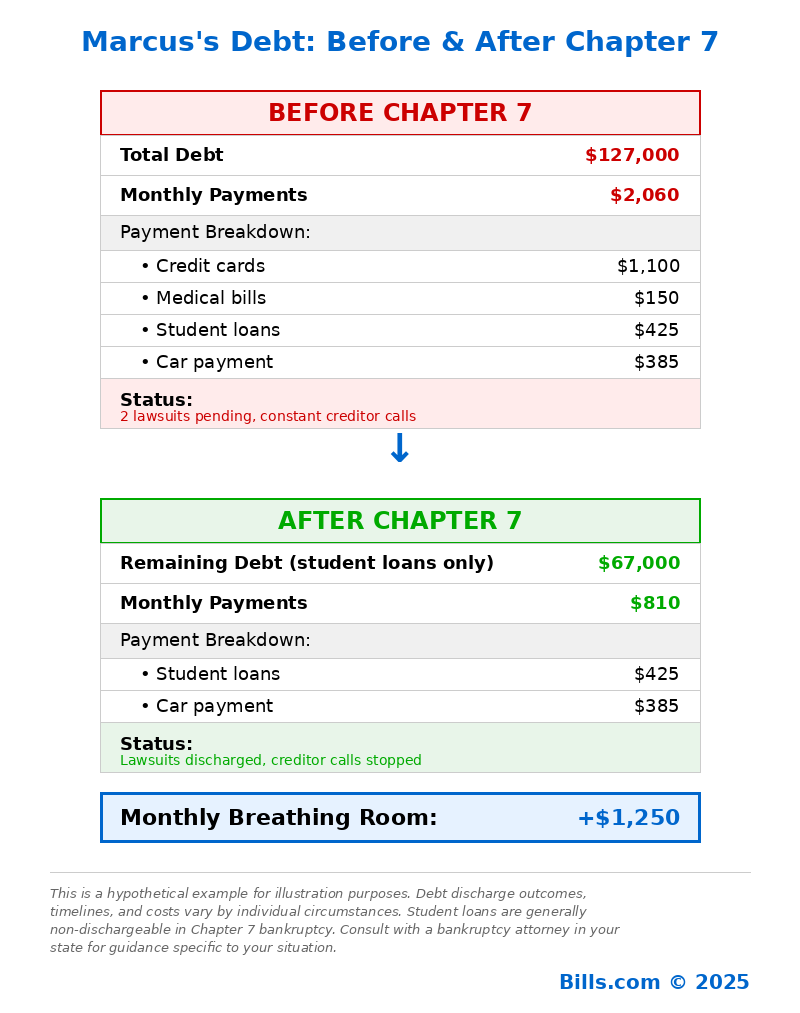

Marcus passed the Chapter 7 means test because his six-month income average fell below Ohio's median for a household of two. Teachers on 10-month pay cycles often qualify because the means test includes summer months with zero paychecks. His $67,000 in student loans won't be discharged, but eliminating $60,000 in other debt will drop his monthly payments from $2,060 to $810—giving him $1,250 in monthly breathing room.

Table of Contents

Marcus sat at his desk in the spare bedroom that doubled as his home office, a stack of ungraded history papers pushed to one side. In their place: credit card statements, medical bills, and a certified letter from an attorney representing one of his creditors.

The numbers made his stomach turn every time he looked at them.

This real-life example shows how the Chapter 7 means test works in practice—using a teacher's simulated income, debts, and timeline.

Credit cards: $52,000. Most of it came from just trying to survive—maxing out cards to cover groceries, unexpected car repairs, childcare gaps, and regular bills when money got tight. Medical debt: $8,000 from when the family dog had emergency bloat surgery last year. The vet saved the dog's life, but the bill was devastating.

Student loans: $67,000 from his bachelor's and master's degrees in education.

Total debt: $127,000. Annual salary: $58,000.

Marcus had been putting off the bankruptcy conversation for months, but two creditors were threatening lawsuits and he couldn't keep juggling minimum payments. The question weighing on him: Does someone with a professional job and a $58K salary even qualify for Chapter 7 bankruptcy?

He owned a 2019 Honda Civic with about $6,000 in equity. He had a small 403(b) retirement account through the school district with roughly $18,000. He rented his apartment—no house. His savings account held about $900. Would the bankruptcy court take these assets? And more importantly, would his income disqualify him from Chapter 7 entirely?

Let's walk through Marcus's actual means test calculation to find out.

Marcus's income: is $58,000 too much?

Marcus's first concern was straightforward: his teaching salary was $58,000 a year. When he looked up Ohio's median income for a household of two—him and his daughter—the number was $81,578 annually as of November 2025, or $6,798 monthly.

The Chapter 7 means test is a calculation the bankruptcy court uses to determine if you have enough disposable income to repay your debts. It compares your income to your state's median income for your household size. If you're below the median, you typically qualify for Chapter 7 without further analysis.

At first glance, Marcus looked like he was below the median. But his attorney explained something Marcus hadn't considered: the means test doesn't look at your annual salary or your current paycheck. It looks at your average income over the past six calendar months.

For Marcus, that meant May through October 2024. And here's where teaching pay cycles complicated things: Marcus's district paid teachers on a 10-month schedule. His annual $58,000 salary was divided across ten months only—not twelve. That meant his monthly gross pay during the school year was $5,800, but in July and August he received zero paychecks.

Here's what his six-month average actually looked like:

- May 2024: $5,800

- June 2024: $5,800

- July 2024: $0 (no paycheck)

- August 2024: $0 (no paycheck)

- September 2024: $5,800

- October 2024: $5,800

Total: $23,200 ÷ 6 months = $3,867 per month average.

That number—$3,867—was well below Ohio's median of $6,798 for a household of two. Marcus passed the first step of the means test. Because his six-month average income fell below the state median for his household size, he didn't need to fill out the complicated expense calculation. He qualified for Chapter 7 based on income alone.

Why middle-income professionals often qualify:

- Household size raises the income threshold (single parents often benefit)

- Irregular pay cycles (like 10-month teaching contracts) matter more than annual salary

- Job title is irrelevant—the means test looks only at income and necessities

The student loan question everyone asks

Marcus's biggest single debt was his student loans—$67,000. When he first considered bankruptcy, that's what kept him up at night. If Chapter 7 couldn't wipe out his student loans, what was the point?

The truth is: Chapter 7 bankruptcy won't discharge his student loans. Federal student loans (and most private ones) survive bankruptcy except in cases of extreme, permanent hardship, which is difficult to prove. Marcus will still owe that $67,000 after his bankruptcy case is complete.

But here's what mattered: Having student loans didn't disqualify Marcus from filing Chapter 7. The means test asks whether you can afford to pay back your credit cards, medical bills, and other unsecured consumer debts.

For Marcus, the math was straightforward. His current minimum debt payments:

- Credit card minimums: $1,100/month (and climbing as he fell behind)

- Medical bill payment plan: $150/month

- Student loan payment: $425/month (income-driven repayment)

- Car payment: $385/month

Total monthly payments: $2,060.

After Chapter 7, his credit card debt and medical bills would be discharged. His monthly payments would drop to $810—just his student loan and car payment. That's $1,250 less each month, money he could use for rent, groceries, childcare, and the unexpected expenses that come with raising a kid as a single parent.

What gets wiped out vs. what stays

One of the first things Marcus wanted to understand was exactly what would happen to each of his debts. His attorney walked him through it with specific numbers.

Debts that will be discharged (gone forever):

- $52,000 in credit card debt → $0

- $8,000 in medical bills → $0

- Total relief: $60,000 eliminated

Debts that won't be discharged (still owed):

- $67,000 student loans → Remains

- Car loan → Remains (if he wants to keep the car)

The before and after:

Before Chapter 7:

- Total debt: $127,000

- Monthly payments: $2,060

- Creditor calls: Constant

- Lawsuits: Two pending

After Chapter 7:

- Remaining debt: $67,000 (student loans only)

- Monthly payments: $810 (student loans + car)

- Creditor calls: Stopped by automatic stay

- Lawsuits: Dismissed

- Monthly breathing room: $1,250

That extra $1,250 a month changes everything. Marcus can build a small emergency fund so a car repair doesn't trigger another crisis. He can afford his daughter's school supplies without stress. When his daughter's class announces a field trip, he doesn't have to weigh it against the electric bill.

Marcus's decision and what happened next

Once the numbers were clear, the question stopped being "Can I?" and became "What happens next?"

His attorney explained the timeline and what to expect.

November 2024: filing

Marcus filed his Chapter 7 petition. The filing fee was $338, and his attorney's fees were $1,500, which he'd been paying down in installments over the previous three months. As soon as the petition was filed, the automatic stay went into effect. An automatic stay is a temporary court order that blocks creditors from pursuing you for payment. The creditor calls stopped immediately. The pending lawsuits were halted.

December 2024: the 341 meeting

About five weeks after filing, Marcus attended the 341 meeting of creditors. That’s a meeting where creditors are allowed to contest your bankruptcy, but they rarely do. It lasted less than ten minutes. The trustee asked him basic questions about his income, assets, and debts. He'd been nervous, but it was straightforward. None of his creditors showed up.

Assets and exemptions

Marcus didn't own a home—he rented his apartment. His Honda Civic had about $4,500 in equity, which was fully protected by Ohio's motor vehicle exemption (up to $5,025 as of April 2025).

His 403(b) retirement account with $18,000 was protected—retirement accounts are generally exempt in bankruptcy. His small savings account (about $900) fell within Ohio's wildcard exemption. The trustee determined it was a no-asset case, meaning nothing would be sold to pay creditors.

March 2025: discharge

About four months after filing, Marcus received his discharge order. The $52,000 in credit card debt was gone. The $8,000 in medical bills was eliminated. He still owed his student loans and his car payment, but his total debt had dropped from $127,000 to roughly $75,000 (student loans plus remaining car balance).

His life now

Marcus's credit score took a hit—it dropped from around 600 to 540. But he's already rebuilding his credit. He opened a secured credit card and uses it for gas, paying it off every month. The Chapter 7 bankruptcy will stay on his credit report for ten years, but the impact lessens over time.

More importantly, he can breathe. When his daughter's class announced a field trip to the state capitol, he signed the permission slip without hesitation. When his car needed new tires, he didn't panic. He built up a $1,400 emergency fund in his first six months post-discharge.

He still teaches high school history. He still has student loans to pay off over the next decade. But he's not drowning anymore. Chapter 7 didn't give him a blank slate—it gave him breathing room. And sometimes, breathing room is everything.

Bills Action Plan

If you're in a similar situation:

Step 1: Calculate your 6-month income average

Add up your gross income (before taxes) from the past six full calendar months and divide by six. Include all income sources: wages, bonuses, rental income, unemployment. Don't include Social Security or VA disability benefits. If you're a teacher on a 10-month pay cycle, those zero-paycheck summer months count in your average.

Step 2: Look up your state's median income

Go to justice.gov/ust/means-testing and find the current median income for your state and household size. Make sure you're using the most recent data—the numbers update twice a year.

Step 3: Compare your income to the median

If your average is below your state's median, you likely qualify for Chapter 7 based on income. If you're above the median, you'll need to complete a more detailed expense calculation—talk to a bankruptcy attorney about this step.

Step 4: List your debts by type

Identify which debts can be discharged (credit cards, medical bills, personal loans) and which typically can't (student loans, recent taxes, child support, secured debts like car and home loans if you want to keep the property).

Step 5: Calculate your potential monthly payment reduction

Add up what you're currently paying toward dischargeable debts each month. That's roughly how much breathing room Chapter 7 could create in your budget.

Step 6: Consult with a bankruptcy attorney

Most bankruptcy attorneys offer free consultations. They can review your specific situation, explain which debts can be discharged, discuss timing considerations, and help you understand whether Chapter 7 or another option makes sense for your circumstances.

Free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Actual client of Freedom Debt Relief. Client’s endorsement is a paid testimonial. Individual results are not typical and will vary.