Chapter 7 Bankruptcy Qualifications: Complete Means Test Guide

Bills Bottom Line

To qualify for Chapter 7 bankruptcy, your income must either fall below your state's median for your household size, or—if above the median—you must show minimal disposable income after allowed expenses like mortgage, car payments, taxes, and childcare. The means test looks at your average gross income over the past six months, not your current income. High earners with substantial necessary expenses often still qualify. Even if you pass the means test, you'll also need to pass the asset test. If Chapter 7 doesn't work, Chapter 13 bankruptcy offers an alternative path.

Table of Contents

- What is the Chapter 7 bankruptcy means test?

- Step 1: The income comparison (below median test)

- Step 2: The expense calculation (disposable income test)

- Official forms you'll need to file Chapter 7 bankruptcy

- Special circumstances and exemptions

- Strategic considerations: when to file

- What happens after you pass the means test?

- What to do if you don't qualify for Chapter 7

- Bills Action Plan

Editor Note: This article provides general information only and is not legal advice. Bankruptcy laws and means test calculations vary by state and change regularly. Consult with a bankruptcy attorney in your state for guidance specific to your situation.

Marcus sat at his desk with a stack of bills and a question that kept him up at night: Does someone making $58,000 a year even qualify for Chapter 7 bankruptcy?

The 34-year-old high school history teacher had significant credit card and medical debt, plus student loans totaling around $127,000. His salary wasn't poverty-level, but creditors were threatening lawsuits. Could a single dad with a teaching salary actually qualify?

The answer surprised him. Let's walk through how the Chapter 7 bankruptcy means test actually works.

What is the Chapter 7 bankruptcy means test?

The Chapter 7 means test determines whether you qualify for Chapter 7 bankruptcy based on your income and expenses. Congress created it in 2005 through the Bankruptcy Abuse Prevention and Consumer Protection Act to prevent people with significant disposable income from wiping out debts they could otherwise repay.

The test works in two steps:

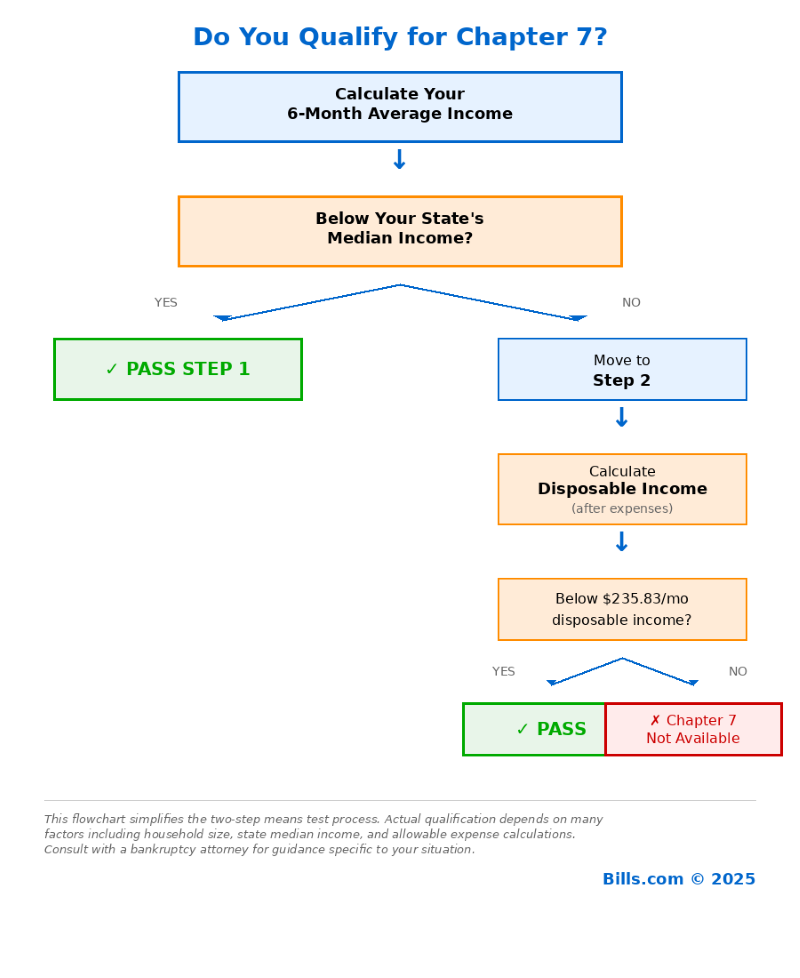

Step 1: Income comparison. If your average monthly income over the past six months falls below your state's median income for your household size, you automatically pass. No further calculation needed.

Step 2: Expense calculation. If your income exceeds the state median, you must calculate your disposable income after subtracting allowed expenses. If your disposable income is low enough, you can still qualify.

Most people who file Chapter 7 ultimately qualify, particularly those with below-median income or necessary living expenses that reduce their disposable income.

Who has to take the means test?

Most people filing Chapter 7 must take the means test. Certain filers are exempt:

- Disabled veterans with a VA disability rating of 30% or higher, if debts were incurred primarily during active duty

- Reservists and National Guard called to active duty for at least 90 days after September 11, 2001

- Business debt filers whose debts are more than 50% business-related rather than consumer debt

What happens if you pass vs. fail the means test?

If you pass, you can proceed with your Chapter 7 case. The court will still review your assets and overall financial situation, but passing the means test is the first major hurdle.

If you fail, you typically cannot file Chapter 7. Your case would be dismissed, or the court might convert it to Chapter 13 bankruptcy, which involves a 3-5 year repayment plan.

Step 1: The income comparison (below median test)

This is where most people either pass quickly or move to Step 2. The question: Is your average monthly income over the past six months below your state's median income for your household size?

If yes, you're done. You qualify for Chapter 7 based on income alone. If no, you'll complete the expense calculation in Step 2.

What counts as income?

The means test uses your average gross monthly income over the six full calendar months before filing. This includes:

- Wages, salaries, tips, bonuses, overtime, commissions (before taxes)

- Business income, rental income, interest, dividends

- Pension, retirement income, unemployment, workers' compensation

- Regular contributions from others (spouse, partner)

What doesn't count: Social Security benefits (including SSDI and SSI), VA disability benefits, certain crime victim payments.

This matters. If significant income comes from Social Security or VA disability, your means test income may be much lower than your actual monthly income.

The 6-month lookback period

The means test uses the six full calendar months immediately before the month you file. If you file March 15, the test looks at September through February.

This lookback period can work in your favor. If your income recently dropped—job loss, reduced hours—the six-month average may be lower than your current income. If you recently got a raise or bonus, it might push your average higher temporarily.

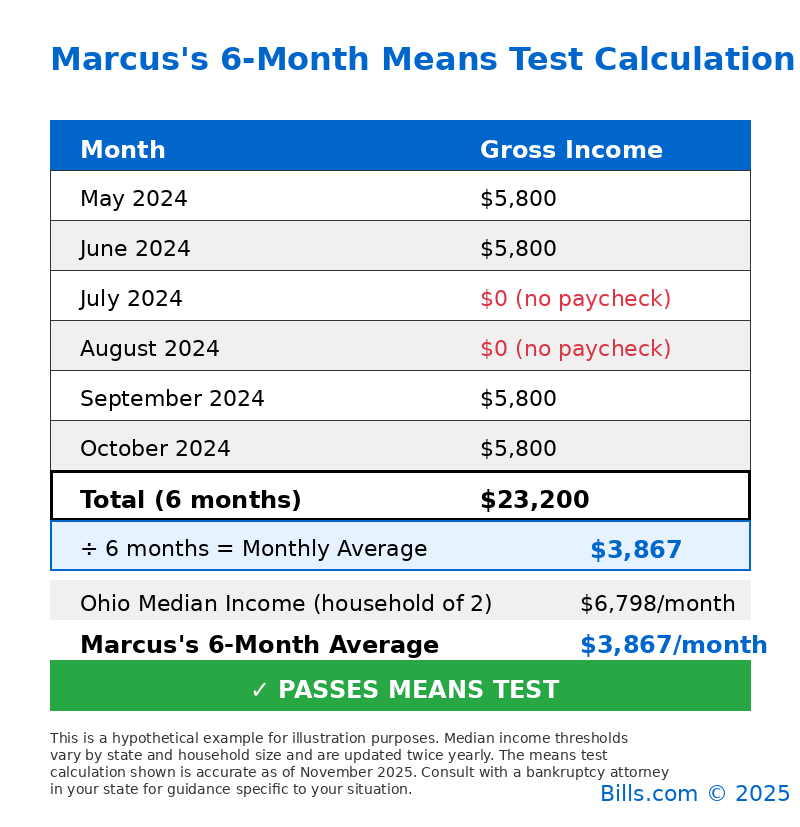

For Marcus, the lookback period made a significant difference. His district paid teachers on a 10-month schedule. His annual $58,000 salary was divided across ten months ($5,800 per month during school year), but his six-month average was just $3,867 because it included July and August—two months with zero paychecks.

How household size affects qualification

Median income thresholds increase with household size. A single person in California might need income below $77,000, while a family of four might qualify with income up to $135,000.

Household size includes you, your spouse (if filing jointly or living together), your dependents, and anyone else you support financially.

Marcus's household size was two: him and his 8-year-old daughter. Ohio's median for a household of two was $68,686 annually ($5,724 monthly) as of November 2025. His six-month average of $3,867 fell well below that threshold. He passed Step 1.

Median income figures update twice a year (May 1 and November 1). Always check current numbers for your state at justice.gov/ust/means-testing.

Step 2: The expense calculation (disposable income test)

If your income is above your state's median, you move to Step 2: the expense calculation. The goal is to determine your monthly disposable income—what's left after necessary living expenses.

If your disposable income is below $171 per month, you pass. If it's above $285, you fail (based on the means test form effective April 1, 2025). In between, the court will impose a sliding scale based on how much unsecured debt you could repay over five years.

Allowable expense categories

The means test uses standardized expenses from the IRS called Collection Financial Standards, combined with your actual expenses for certain categories. Allowable expenses include:

- Housing and utilities: Mortgage/rent, property taxes, insurance, electricity, gas, water, phone, internet. Some use IRS standards; others use actual expenses.

- Transportation: Car payments, insurance, gas, maintenance. IRS has national and local standards for ownership and operating costs.

- Food, clothing, personal care: IRS national standards based on household size.

- Healthcare: Insurance premiums, out-of-pocket medical expenses, prescriptions.

- Taxes and mandatory deductions: Federal, state, local taxes, retirement contributions required by employer.

- Secured debts: Mortgage, car loans—debts secured by property you want to keep.

- Childcare and education: Daycare, after-school care if necessary for employment.

- Child support and alimony: Court-ordered payments.

How the calculation works

The formula:

Monthly disposable income = Current monthly income - allowed expenses-secured debt payments-priority debt payments

Now, multiply your monthly disposable income by 60 to get projected disposable income over five years.

Below $10,275 = pass. Above $17,150 = fail. In between = depends on whether you could repay 25% of unsecured debt.

Common mistakes

Overestimating allowable expenses. You can't list whatever you spend. Most categories use IRS standards. If you spend $2,000 eating out but the IRS food standard is $800, you can only deduct $800.

Forgetting to average irregular income. Variable income must be calculated accurately. One big month can skew results.

Including non-allowable debts. You cannot deduct unsecured credit card payments or medical bills. Only secured debts and priority debts count.

Official forms you'll need to file Chapter 7 bankruptcy

The means test is completed using official bankruptcy forms. Form 122A-1 calculates your income and compares it to your state's median—if you're below, you stop there. If above the median, Form 122A-2 walks through the expense calculation. Disabled veterans and qualifying military members use Form 122A-1Supp instead.

These forms are available at uscourts.gov/forms/bankruptcy-forms. Most people work with a bankruptcy attorney to complete them accurately.

Special circumstances and exemptions

Disabled veterans and military members

If you're a disabled veteran with a VA disability rating of 30% or higher, you're exempt from the means test—but only if your debts were incurred primarily while on active duty or during homeland defense activities. Members of the Reserve or National Guard called to active duty for at least 90 days after September 11, 2001, are also exempt during active duty and for 540 days after returning home.

Business debt exception

If more than 50% of your debt is business-related (not consumer debt), you don't have to take the means test. Business debt includes loans for inventory, commercial leases, business credit cards used exclusively for business. This exemption is common among small business owners and freelancers whose business ventures failed.

Strategic considerations: when to file

Timing your bankruptcy filing strategically is legal and smart. The six-month lookback period creates planning opportunities.

Job loss, pay cuts, or expired bonuses can lower your average over time. Raises or one-time windfalls temporarily inflate it. Waiting for low-income months to enter (or high-income months to exit) the calculation window can make the difference between passing and failing.

However, don't delay filing if creditors are about to garnish wages, repossess property, or foreclose on your home. Sometimes immediate relief matters more than perfect timing. Talk to a bankruptcy attorney about modeling different filing dates.

What happens after you pass the means test?

Passing the means test is a major milestone, but it doesn't guarantee approval. The court still reviews:

The asset consideration: Chapter 7 is liquidation bankruptcy. A trustee can sell non-exempt assets to pay creditors. Each state has exemption laws protecting certain property—home equity up to a limit, one vehicle, retirement accounts, household items. If you have significant non-exempt assets, you may lose them in Chapter 7, though Chapter 13 might be a better option that allows you to keep the property

The trustee's review. The bankruptcy trustee reviews your financial documents, questions you at the 341 meeting of creditors, and determines whether your bankruptcy is filed in good faith. Suspicious activity—transferred assets before filing, incurring debts you couldn't repay, lifestyle mismatched to expenses—may trigger challenges.

Credit counseling. You must complete credit counseling before filing and debtor education after filing. Both courses are available online for $10-$50 each.

If everything proceeds smoothly, you'll receive your discharge order about 4-6 months after filing.

What to do if you don't qualify for Chapter 7

Chapter 13 bankruptcy as an alternative

If you fail the means test, Chapter 7 isn't an option right now. Chapter 13 bankruptcy is a repayment plan lasting 3-5 years. You make monthly payments to a trustee who distributes money to creditors. At plan's end, remaining eligible debts are discharged (forgiven).

Chapter 13 advantages: You can keep non-exempt property, catch up on missed mortgage or car payments while keeping the property, pay back only a fraction of unsecured debt depending on disposable income, and Chapter 13 stays on your credit report for 7 years vs. Chapter 7's ten years.

The downside: you're in bankruptcy longer and must make regular payments. Missing payments can lead to dismissal (your case ends with no debt forgiveness).

Other debt relief options

If bankruptcy isn't the right fit:

- Debt settlement: Negotiate to pay less than full balance

- Debt management plan: Work with credit counseling agency to consolidate payments

- Debt consolidation loan: Combine debts into one lower-interest loan

- Wait and refile: If your situation is temporary, you might qualify later

A bankruptcy attorney can help you evaluate which path makes sense for your situation.

Bills Action Plan

Here are some practical steps to take to check.

Step 1: Gather your income records: Collect paystubs or income documentation for the past six full calendar months. Include all income sources except Social Security and VA disability.

Step 2: Calculate your average monthly income: Add up your gross income from all six months and divide by six.

Step 3: Look up your state's median income: Visit justice.gov/ust/means-testing for current numbers (updated May 1 and November 1).

Step 4: Compare your income to the median: Below the median = you pass. Above = you'll need the expense calculation.

Step 5: List your expenses if above median: Gather documentation for housing, transportation, healthcare, childcare, taxes, and secured debts. Use Form 122A-2 to calculate disposable income.

Step 6: Consult with a bankruptcy attorney: Most offer free consultations. Bring income documentation, expense records, and debt information.

Free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Actual client of Freedom Debt Relief. Client’s endorsement is a paid testimonial. Individual results are not typical and will vary.

Can I pass the means test if I make $100,000 a year?

Maybe. If you have a larger household size, high necessary expenses (mortgage, car payments, childcare, medical costs), and significant secured debts, you could still qualify. A family of five in a high-cost area with $100,000 income might pass, while a single person with no dependents likely wouldn't. It's highly individualized.

Does Social Security income count?

No. Social Security retirement, SSDI, and SSI are excluded from the means test. This significantly lowers your current monthly income if a large portion comes from these sources.

What if my income varies month to month?

You still calculate the six-month average. Freelancers, commissioned salespeople, seasonal workers—anyone with irregular income adds up all income from the six months and divides by six. Timing your filing strategically can help if you had several low months.

Do I include my spouse's income if we're not filing together?

Usually, yes. If you're married and living together, your spouse's income generally must be included, even if only one spouse files. However, you can exclude income your spouse uses for their own separate expenses. This gets complex—consult a bankruptcy attorney.

What happens if I lie on the means test?

Lying on bankruptcy forms is perjury, a federal crime punishable by fines and prison. The trustee reviews your paperwork carefully, cross-checks with tax returns and bank statements, and questions you under oath. If caught lying, your case will be dismissed, you could be barred from refiling, and you may face criminal charges.

Can I deduct my student loan payments?

No. Student loan payments are unsecured debt and cannot be deducted in the expense calculation. Only secured debts (mortgages, car loans) and priority debts (recent taxes, child support) can be deducted.

If I just lost my job, should I wait before filing?

It depends. If you can cover living expenses while waiting, then yes—waiting can lower your six-month average. However, if creditors are threatening lawsuits, garnishments, or foreclosure, you may need immediate relief. Talk to an attorney about your specific timeline and risks.