Facts & Figure About Student Loans (Video)

- In 2001 the cost of a year of college was $17,377. Today, it is $28,500.

- Student loan debt totaled $1.1 trillion in 2011.

- Consider a 529 savings plan as a tax-free way to save for college.

Learn Trends, Facts and Figures About Student Loans

Financing college, university, and professional training is an expensive undertaking. Bills.com is here to provide you with relevant information about getting a student loan and managing a student loan.

The Big Picture

Here are key facts about student loan debt today:

- Total student loan debt is estimated to be $1.1 trillion, as of 2011. According to a 2010 report by Sallie Mae, the largest private student loan lender, the outstanding balance of Federal Student Loans totals $759 billion.

- Total college and university expenditures totaled $461 billion, or about 3.9% of the 2009 US gross domestic product.

- In 2007, the maximum federal student loan size increased. Since then, there has been a sharp increase in federal student loans, and a marked decrease in private student loans.

- Total federal loans for the 2010-2011 academic year were $103.9 billion vs. private loans totaling $8 billion.

- The number of new delinquent student loan borrowers is on the rise since 2007. According to the Dept of Education, out of 3.6 million borrowers who had their first payments due between October 1, 2008 and September 30, 2009, 326,000 defaulted before September 2010.

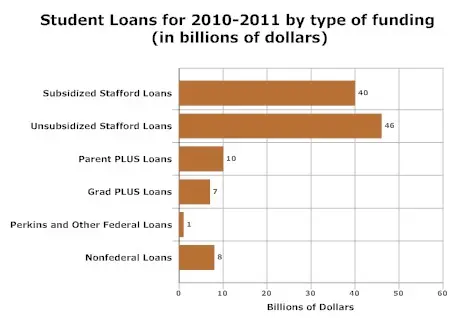

According to the College Board, school loans, both federal and private, for the 2011 academic year totaled approximately $112 billion. The chart below shows how these were divided into five categories, with the unsubsidized Stafford Loans, the largest amount,($46 billion — 41% of loans) followed by subsidized Stafford Loans ($40 billion — 35% of loans) and non-federal loans ($8 billion — 7% of loans).

Costs of Education

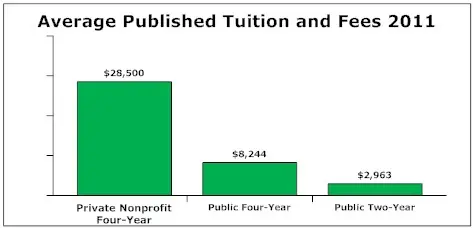

College and university costs keep increasing across the board, for tuition, books, and living costs. Costs vary, depending on the type of the institution. A two-year institution is much cheaper than a four-year one, and a public state college or university is cheaper than private schooling. Private, four-year institutions’ fees and costs have increased at an annual rate of 5.4%, over the last ten years, adjusted for inflation. In 2001 the annual cost was $17,377 and today is $28,500. The chart below illustrates the 2011 cost of education for the various institutions:

Types of Funding for School Loans

Post-high school education is an important life event, and should be planned for in advance. Choosing the best way to finance an education is complicated. Here are the major ways student expenses can be financed:

- Savings or family assets

- Current income

- Grants

- Scholarships

- Federal student loans

- Private student loans

- Institutional loans

Taking a Student Loan

Start planning for your family’s education needs early. If you do not, you reduce your options and can increase your costs. For example, there are specific savings plans with tax advantages, such as the 529 college savings plan and some states offer guaranteed, reduced education costs if you invest early. Before you take out any loans, budget your costs carefully, comparing them to your income and assets. Check your eligibility for grants or scholarships. Do not take out private student loans, before you are sure that you have utilized all available federal student loans, both subsidized federal loans and unsubsidized student loans.

Managing a Student Loan

Taking out student loans is only the first step in a long-term relationship between you and your lender. Once you are required to begin making payments, and when this happens varies from loan to loan, there are a number of factors you have to deal with. For instance, depending on your ability to repay your loans as agreed, you may have to deal with issues like forbearance, deferment, and Income Based Repayment (IBR). You might need to cope with payments which are beyond your ability to pay. Since bankruptcy is not an available option for most student loan debt, it is wise for you to learn about the benefits of consulting student loans and how best to handle student loans in default.

Bills.com student loan section offers, relevant and helpful information covering diverse student loan topics. Here are a few of the topics that we cover:

- How to find a student loan

- Consolidating student loans

- Refinancing student loans

- Wage garnishments and student loans

Use Bills.com as your resource for finding and managing student loans.