- Mortgage lenders evaluate you based on your creditworthiness and LTV.

- A large down-payment and a lower LTV will save you money.

- Learn about the different types of loans based on different LTVs.

LTV: Loan to Value - Learn to Build Equity

Buying a home is a big investment. Your home is likely the biggest single asset you will own. Taking a mortgage loan requires preparation, whether your loan is to purchase a home or refinance your current mortgage. No matter what type of mortgage loan you take, your lender will be sure to evaluate your credit worthiness and the value of your home.

A loan-to-value ratio (LTV) is the amount of loan you take as a percentage of your property’s value. When you purchase a home, the larger your down-payment, the lower your LTV will be. As time goes by, your LTV will be influenced by the changes in the value of your home and the balance of your loan. Make it your financial goal to build equity in your house by reducing your LTV.

Your LTV is very important because it affects your mortgage interest rate and your eligibility. A general rule of thumb for conventional mortgages is that you need an LTV under 80%. However, with mortgage insurance or special loan programs you can obtain a purchase mortgage loan or refinance your mortgage loan even with an LTV above 80%.

To understand loan-to-value and its impact on your taking a mortgage, learn the following:

- Loan-to-Value Definition

- Loan-to-Value and Types of Mortgages

- Loan-to-Value and Mortgage Tips

Loan to Value Defined

LTV is a term used in any loan that is guaranteed by an asset. The most common usage of loan-to-value is for auto loans and mortgage loans. The term refers to the amount of money you owe, in percentage terms, based on the value of the property. Check out the following formula to calculate out your LTV:

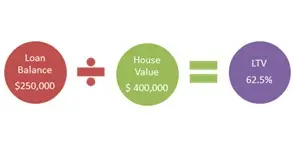

- Loan Balance: The amount you plan on borrowing or the amount you currently owe on your loan.

- House Value: For a purchase mortgage, the lender uses the lower amount between the purchase price or appraised value. Note that a property's taxable value, as set by a county appraiser, may not be an accurate value for LTV purposes.

Here is an example of a borrower with a 62.5% LTV:

Combined Loan to Value ratio (CLTV): Sometimes borrowers take out more than one mortgage loan against the same property. If you take out a second mortgage, then compute your LTV for each loan separately. Your CLTV is the sum of the two LTVs. Here is an example of a borrower with a house worth $225,000 (according to an appraisal report done for a bank):

| Value | LTV | |

|---|---|---|

| First Mortgage | $157,500 | LTV=70% |

| Second Mortgage | $ 45,000 | LTV-20% |

| Total Loan | $202,500 | CLTV=90% |

Quick tip #1

Check out today’s mortgage rates.

LTV and Types of Mortgages

Lenders rely on your credit worthiness to grant you a loan. That means that they check your credit score and your income and debt-to-income ratio (DTI). However, a lender grants a mortgage loan with the additional security of your home. That means, if you don’t pay and default on the loan, then the lender can foreclose on your property and the proceeds of the sale will go towards paying off the loan.

To lower their risks, lenders sometimes require a higher down-payment, when you’re purchasing a home, or more equity for a refinance loan (the amount you would get after selling the property and paying back the loan). Most lenders require that you have a LTV of 80%. Some lenders have less strict rules if you have a higher income, lower monthly debt payment and/or other compensating factors, such as a large investment portfolio.

However, if you want to take more than 80% financing for a purchase loan, then your will need to look into one of these solutions:

- Mortgage Insurance (MI): You can take out a loan up to 95% LTV if you take out MI. In most cases your lender will automatically cancel your MI when you LTV reaches 78% based on your original loan schedule. If your home goes up in value or you pay down your balance to a 80% LTV you can request that the lender terminate the MI. In any case, if your LTV drops you can try to refinance without MI.

- FHA loan: FHA loans are available up to 96.5% LTV. That means you only have to make a small down-payment. However, FHA loans have hefty Mortgage Insurance Premiums (MIP).

- VA loans: If you are an eligible veteran, then look into a VA loan. VA loans do not require MI, and you can obtain up to 100% financing.

If you want to refinance with a high LTV, then you can look into one of these options:

- LTV between 80-95%: Conventional loans with MI and FHA loans.

- LTV over 100%: If your LTV is greater than 100% then you should read more about the eligibility requirements for one of the specific refinance programs for underwater borrowers:

- HARP refinance loan for a Fannie Mae or Freddie Mac loan.

- FHA streamline refinance loan for a FHA loan.

- VA IRRRL for a VA loan.

- HARP 3 proposals.

LTV — Your Financial Plan and Your Mortgage

LTV is a key indicator for the mortgage lender. It is also a useful tool for you to keep track of your equity position in your home. Your financial plan should include building an investment portfolio for your retirement. Although your home is primarily a place to live, it is also a long-term investment. Your goal should be to retire with a 0% LTV, namely to own a home without a mortgage. For some, it is possible to then downsize, selling your paid-off home and buying a less expensive home while pocketing some cash.

Here are a few tips for your financial plan:

- Save money for you down-payment. Make an effort to take a smaller loan and keep your LTV down. You will save a lot of money if you avoid MI.

- Make sure that the monthly mortgage payments are within your budget — and that you establish a rainy day fund to cover all your expenses, including your mortgage payment, for six months. Check out the maximum loan you can afford based on your downpayment, LTV, and DTI. However, you don’t have to max out.

- Avoid using your home as a source of income. Once you have built up equity, don’t rush out to take a cash-out refinance mortgage loan. If rates drop, then refinance to lower your total costs to pay off your mortgage. Use Bills.com mortgage refinance calculator to see today’s rates and your possible savings.

- If you need to consolidate your debt make sure that your financial position is strong enough to meet the payments. Don’t pay off old credit card debt and then run up new bills.

- Home improvements do not usually increase the value of your house at the same level as your investment. If you finance the improvements, consider the realistic impact on your LTV.

Learn From the Past

As many as 11 million borrowers are underwater with LTVs more than 100%. (That means a negative equity position.) Although you don’t have control over a drop in housing prices, you do have control over the balance of your loan. Many borrowers refinanced their loans and kept taking out cash. Even though it looked like their LTV was not increasing — and often decreasing — this was due to an increase in the market. When the housing market soured, their LTVs went through the ceiling. Taking out equity is a risky venture. Make sure you understand how it can affect you. Your house is an important investment and should be a solid one. Monitor your LTV and build your equity.

Quick tip

Use Bills.com mortgage affordability calculator to help you find out the maximum loan you can get based on your income and downpayment.