Steps to Establish Credit

- Establishing credit takes time and good financial habits.

- Take small steps with a secured credit card. Be careful before you co-sign or add as an authorized user.

- Monitor your progress.

- Start your FREE debt assessment

How can I help my daughter establish credit?

My daughter has asked me to get a credit card with her as a joint holder or at least an authorized user as she has no credit. Will this affect negatively my score of at least 750? What's the best option in this situation? She is trying to build up her credit and hopes by having me as the cardholder but her as a joint and paying on time, etc. that it will help. Is this true?

Thank you for your question about establishing credit.

Your daughter is fortunate that you can help her establish credit. This will offer her more alternatives. You are also correct to be concerned about your credit score. Late payments can seriously damage your credit score.

In order to establish credit your daughter needs to have financial activity that is reported on a credit report, including credit cards, retail and gas station cards, installment Loans. Sometimes rent, if reported by the landlord, is also included.

Tip

Even if you don’t have any credit, any negative activity, including delinquent utilities, can be reported. Collection items and public judgments are reported and be a big strike against establishing credit.

Establishing credit is an important financial step. Improper usage of credit cards leads to a low credit score, and creates debt that is hard to payback. Establishing credit takes time and should be done gradually. Your daughter will want to prove to the creditors (and you if you are helping her) that she can responsibly handle debt.

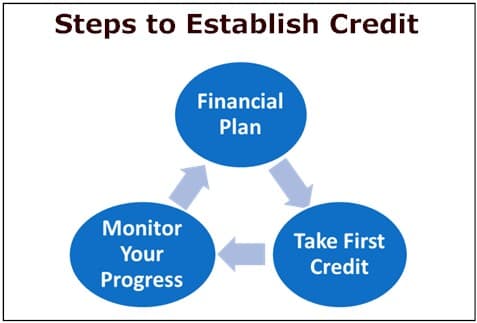

I recommend that she follow these steps:

- Educational Period: Creating good financial habits

- Taking First Credit

- Evaluation and Establishing Credit

Establish Credit: Create Good Financial Habits

In order to establish credit, you daughter should learn how to handle her personal finances in a responsible manner. She can start with these four practical steps:

- Create a Budget: Knowing how much money you make and how you are spending your money sounds trivial. We all know that we can’t spend what we don’t have. However, credit cards make it easier to spend beyond our earning power, until we reach the credit limit, and begin to look for more credit. I recommend that your daughter read Bills.com personal budget guide and concentrate on tracking her monthly expenses. It is time consuming and requires discipline, but making and keeping a budget is an important tool to maintain an healthy financial position.

- Save Money: I recommend that your daughter open a savings account and make monthly deposits. Ideally these deposits would represent 10% of her income and be a beginning of her emergency fund, which ideally should have at least 6 months of living expenses. (The savings fund could also be used for a deposit on her secured credit card). Use Bills.com Saving Machine to help figure out ways to save money.

- Order a credit report: You are entitled to a free credit report from each of the major CRA (Credit Reporting Agencies), TransUnion, Equifax, and Equarian, once a year. I recommend that your daughter order a report from one of these CRAs every 4 months. (To begin with she may want to order one to begin with, then the next one 3 months after taking out her first card, and then rotate every 4 months).

- Learn the components of a credit score: Your credit score is based on your credit history and the most important factors are:

- Timely Payments – Always make your payments on time

- Credit Utilization – Don’t max out on your credit lines. Try to pay off your cards each month, but do not go over 30% of your line of credit on any of your cards.

- Credit Mix – To establish a high credit score, have different types of credit.

Quick Tip #1

You can get your free credit report from www.annualcreditreport.com, however it does not include a credit score. You can get a credit report with your credit score for a free trial period. It is a good idea to monitor your progress, as you take steps to establish your credit score.

Establish Credit – Know What You Are Doing.

You are 100% correct in being worried about the effects on your credit score if you mingle your account with your daughter. All activity is registered on all account holders and/or users. That is a double-edged sword. Any positive activity helps build your credit and any negative activity lowers your credit.

Before you read about some possible solutions, here is a brief explanation of the two possible solutions that you mention:

- Co-sign on her account: Both of you will be account holders and jointly responsible for debt. Any activity will be registered on your credit report and affect your score.

- Ask yourself: how can I make sure the payments will be made on time?

- Add her as an authorized user: Only you will be responsible for the debt, although your daughter can run up debt based on your credit limit.

- Ask yourself: how can I make sure she doesn’t abuse the card?

The two main problems that need to be addressed are timely payments and abuse of card. Hopefully, after following the four steps listed above, your daughter now has good financial habits and a game plan.

Her next steps to establish credit are

- Take out a Secured Credit Card: Your daughter can use her savings as a deposit for a secured card. She should speak to her local bank or credit union about getting a card. Wells Fargo offers a Secured Card between $300-$10,000. However, their interest rate (July 2012 rates) is a whopping 18.99% for purchases and more for cash or overdraft advances. Remember rule number one: Make your payments on time and charge only what you can afford to pay. Keep the credit line small and affordable. The rest of your funds keep in a separate account. If you daughter needs help starting the account (and this is not a good beginning sign), then you consider lending her the money. This will limit your exposure to a one time loan and help your daughter limit her exposure. If she doesn’t wisely use her credit line, then the funds in the account can be taken by the bank to pay off her debt.

- Cosign on an unsecured credit card or personal loan: I do not recommend cosigning a loan, unless you are prepared to actually pay for the loan. A co-signer has 100% responsibility for the entire loan. Also, if the strong borrower does not control the payments, then they risk the possibility that payments aren’t made on time and their credit score is damaged. If you go this line, then I recommend that you either make the payments from your own account or make arrangements to receive confirmation of the monthly payments. If they are not promptly made, then make sure you have enough time to make them without any penalties.

- Add your daughter as an authorized user: Since the card is in your name, you have sole responsibility for the payments. You do face the risk that your daughter will misuse the card. I recommend that you use a card that allows you to limit the credit limit on an authorized card. Remember to monitor your bills.

- Get a Retail card: Your daughter can apply for a retail card or gas station card. However, she should only do so for a store that she regularly uses. She should not run up charges for rewards or points, but only for items she can afford to pay off with cash. In order to establish credit, she needs to make charges AND pay them off. In order to avoid expensive interest charges, paying them off in full is best.

Establishing Credit: An Ongoing Process

It is impossible to establish credit overnight. Your credit score is determined by your credit history. It takes time for activity to be reported, and it is virtually impossible to obtain a wide variety of credit overnight.

However, by patiently taking out credit and paying it back on time, your daughter will build up her credit history. By having a game plan, and following her budget, she will learn not to overcharge. Credit cards have high interest rates, and anything charged and paid back over time adds a lot of expense to the original purchase. (Avoid the minimum payment cycle).

Remember, to establish credit, follow these steps:

- Make a game plan. Create and maintain your budget. Keep a savings account.

- Take out credit, starting with a secured card. Make your payments on time and pay off all your charges at the end of the month. Think of it the card as cash. Charge items, only if you have that money in the bank.

- Monitor your credit report and credit score. Make sure that items are being correctly reported and any incorrect items should be disputed.

Quick Tip #2

If you have bad debt and are struggling to meet your minimum payments, then get a free consultation from a Bills.com debt provider. Before rebuilding credit you will need to deal with your current debts.

Free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Actual client of Freedom Debt Relief. Client’s endorsement is a paid testimonial. Individual results are not typical and will vary.