Do Debt Settlement Companies Take Money Upfront?

Bills Bottom Line

It’s illegal for debt settlement companies to charge fees before a debt is settled and you've approved the offer. You pay after results—not before. Bad actors do break this rule, which is exactly why knowing the red flags matters. A legitimate debt settlement company should walk you through what a normal program looks like.

Table of Contents

You read something that made you stop. Maybe it was a Reddit thread, maybe a review site. Someone said debt settlement companies take your money first—thousands of dollars—before they've negotiated a single debt. And the comments agreed. Sham companies were charging for service and delivering zero results, leaving people worse off.

What those posts describe is real. But they describe an industry that the government overhauled in 2010. Debt settlement companies are now held to a higher standard. For one thing, they can’t take money upfront.

Under the FTC's Telemarketing Sales Rule, a for-profit debt settlement company cannot charge you money until it successfully reaches a deal, you approve it, and you make a payment toward it. That's the law. If a company asks for money before that, walk away. If you're still learning how debt settlement works, start there first.

Can debt settlement companies charge fees upfront?

No. Federal law says taking money upfront is illegal.

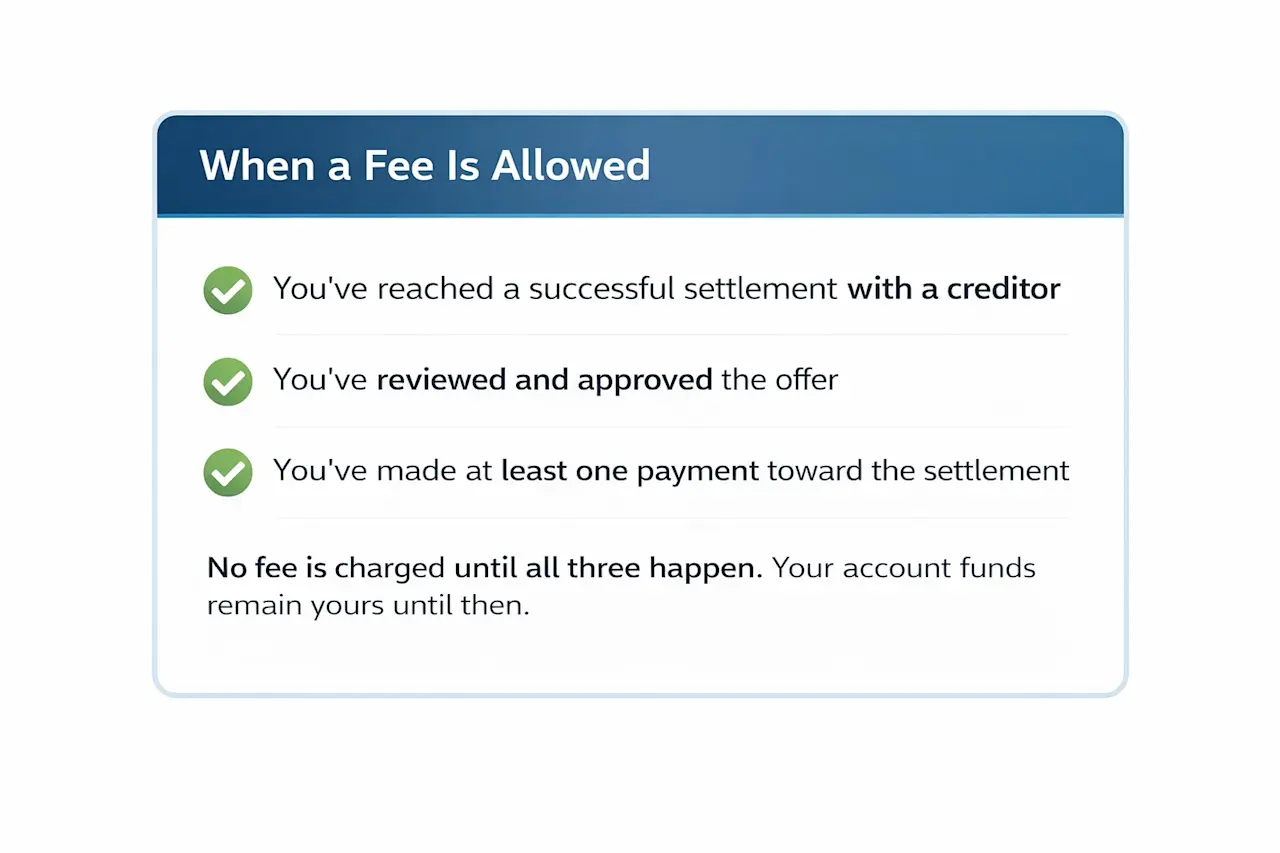

In 2010, the FTC updated its Telemarketing Sales Rule to ban debt settlement companies from collecting any fees before delivering results. The rule applies to for-profit companies that use telemarketing to reach clients, which covers most debt settlement companies you’d work with.

Here's what the rule actually requires before any fee can be charged:

That dedicated account matters. During the program, you build savings in an account you own and control. The debt settlement company can’t touch those funds for fees until it has delivered meaningful results.

Fees you might miss: The dedicated account itself typically carries a small monthly fee, around $10 per month. This is charged by the third-party company managing your account (the bank, in other words), not the debt settlement company. There's usually a one-time setup fee in a similar range as well. These smaller fees are separate from the company's settlement fees, and you should get them in writing before you enroll. If they aren't disclosed upfront, ask.

Legitimate debt settlement company fees are also real and significant, typically 20-25% of enrolled debt. Regardless of fee size, settlement fees and account fees aren’t collectible by the debt settlement company until they’ve successfully negotiated your debt. At most, they can ask you to put money toward fees into your dedicated account, which you can withdraw any time.

The confusion around this rule has a clear history. Which is exactly why the fear keeps circulating.

Why people say debt settlement companies take money upfront

The skepticism isn't irrational. It comes from three places, and each one is legitimate.

Many settlement companies charged upfront fees before 2010

Before the FTC rule took effect on October 27, 2010, charging large upfront fees was standard practice in the debt settlement industry. The FTC documented 236 enforcement actions in the decade before the rule—real cases, real harm, real money lost.

After the rule took effect, roughly 80% of debt settlement companies exited the market. The companies that survived had to change how they operated.

Attorney fees are sometimes confused with debt relief company fees

Some people encounter debt settlement attorneys charging retainers or hourly fees for debt-related legal work and assume the same rules apply to all debt help services. They don't.

Attorneys who meet you in person before you enroll in a debt settlement program may be allowed to charge you upfront fees. Attorneys may also charge separately for actual legal defense work—like responding to a lawsuit—which is legal services, not debt relief services. Legal services fall outside the advance fee ban.

A note on attorney fees: Whether an attorney can charge upfront fees for debt-related services depends on how they engage with you and state bar rules. If you're thinking about working with an attorney, ask directly how and when their fees are charged.

Some debt settlement companies are still breaking the law and being punished

In July 2025, the FTC took action against Accelerated Debt Settlement over an alleged $100 million scheme charging illegal upfront fees. The law is clear. Some companies break it anyway. That's why enforcement exists, why verification matters.

How to find a legitimate debt settlement company

Some debt settlement companies are legitimate. You don't have to take a company's word for it. Here's how to check.

- Talk to a debt settlement company first. A legitimate company will clearly explain that no fees are charged until a specific debt is settled, you've approved the offer, and at least one payment has been made. They'll put it in writing. If the fee structure is vague, verbal only, or pressured—that's a red flag. Walk away if the company smells fishy.

- Check state websites. Many states require debt settlement companies to be licensed. Check your state attorney general's website or ask the company directly for their license number in your state. If they’re listed, that’s a green flag.

- Look for ACDR membership. Members of the Association for Consumer Debt Relief follow the Uniform Disclosure standard, meaning they tell you everything relevant upfront. Membership is a green flag.

- Search the CFPB complaint database. Before you sign anything, search the company's name at consumerfinance.gov/complaint. Look at what people are complaining about, not just whether complaints exist. Details might be relevant.

Know the red flags. Walk away if any of these appear:

Debt Settlement Company Red Flags

Red flags—walk away if you see any of these:

- Debt settlement fee is requested before a settlement is reached

- Specific savings amounts or timelines are 100% guaranteed

- You're pressured to sign immediately or told an offer expires

- No written contract, or the contract doesn't clearly state when fees are charged

- The company can't or won't tell you what happens if a creditor sues you during the program

Before committing, it's also worth understanding the full pros and cons of debt settlement, including what happens to your credit and how long the process typically takes.

One more thing worth asking: some debt settlement companies connect clients with attorneys if a company you owe sues you during the program. Ask any debt settlement company you're considering whether this is part of their service, and what it costs. Some won’t offer this service.

Bills Action Plan

- Step 1: Contact a debt settlement company and ask them to walk you through exactly when and how fees are charged, including any dedicated account fees. A legitimate company will have a clear, written answer.

- Step 2: Search your state attorney general's website for licensed debt settlement companies in your state.

- Step 3: Search the company's name at consumerfinance.gov/complaint. Look for patterns that could cost you.

- Step 4: Ask “What happens if a creditor sues me during the program?” The answer tells you a lot.

- Step 5: Get the full fee structure in writing before signing, including settlement fees and any account fees. If it's not in the contract, it doesn't exist.

Free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Actual client of Freedom Debt Relief. Client’s endorsement is a paid testimonial. Individual results are not typical and will vary.

Is it ever legal for a debt settlement company to charge upfront fees?

No, not for companies that use telemarketing to reach clients, which covers the vast majority of the industry. The FTC's Telemarketing Sales Rule makes it illegal to collect any fee before a specific debt is settled, you approve it, and you make at least one payment. If a company is asking for money before any of that happens, they're breaking the law, and you should walk away.

What fees do legitimate debt settlement companies actually charge?

There are two types to know about. Settlement fees typically run 20-25% of the enrolled debt amount, charged per debt resolved, after it’s resolved. So if a company settles a $5,000 credit card for $2,500, their fee would typically be $1,000-$1,250. Separately, the dedicated account you open to hold your funds typically charges a small monthly fee paid to the account administrator, not the debt settlement company. All fees should be disclosed in writing before you enroll. The rule isn't that debt settlement is free—it's that you pay after results.

Can creditors still sue me if I'm in a debt settlement program?

Yes. Enrolling in a debt settlement program does not legally prevent a creditor from filing a lawsuit. Debt settlement typically involves stopping payments to creditors while negotiations are underway, and creditors may sue to recover the debt. This is a real risk you should discuss with any company before enrolling. Some debt settlement companies account for this and will connect you with attorneys if you’re sued during the program. Ask about this directly.

How does debt settlement affect my credit score?

Credit damage is an expected outcome of debt settlement. Most people stop paying creditors during negotiations, and those delinquencies get reported to credit bureaus. Settled accounts also appear on your credit report and may be noted as "settled for less than the full amount." The impact could be meaningful and typically lasts for several years. For a full breakdown, see our guide on how debt relief affects your credit.

Is forgiven debt taxable?

It might be. Forgiven debt is considered taxable income by the IRS. If a creditor forgives $600 or more of your debt, you might receive a Form 1099-C. But even if you don’t receive a tax form, you are required to report the forgiven debt to the IRS on your tax return.

The IRS allows an exception for people who are insolvent. That means that the total of what you owe is greater than the total value of what you own. If you’re insolvent when you settle the debt, you won’t owe federal income tax on the forgiven portion. You might want to talk to a tax professional to understand what debt settlement could cost you in taxes.