When Can a Credit Card Company Sue You?

Bills Bottom Line

A credit card company could take you to court—but lawsuits are usually a last resort. Most legal action happens after about six months of missed payments, and the decision often comes down to how much you owe and whether the creditor believes it can collect. Knowing what triggers a lawsuit—and what to do if one is coming—could help you protect yourself.

Table of Contents

Missing payments on a credit card sets off a predictable chain of events. Calls, letters, collection notices—each one a little more urgent than the last. At some point, you may start wondering whether a lawsuit is next.

That’s a fair question. Credit card companies sue far less often than most people assume. Litigation is expensive and time-consuming, and most creditors would rather collect some money than spend more money chasing it.

That said, lawsuits do happen. Understanding what triggers them matters. Knowing your options puts you in a much stronger position than hoping the phone stops ringing.

How long before a credit card company can sue you?

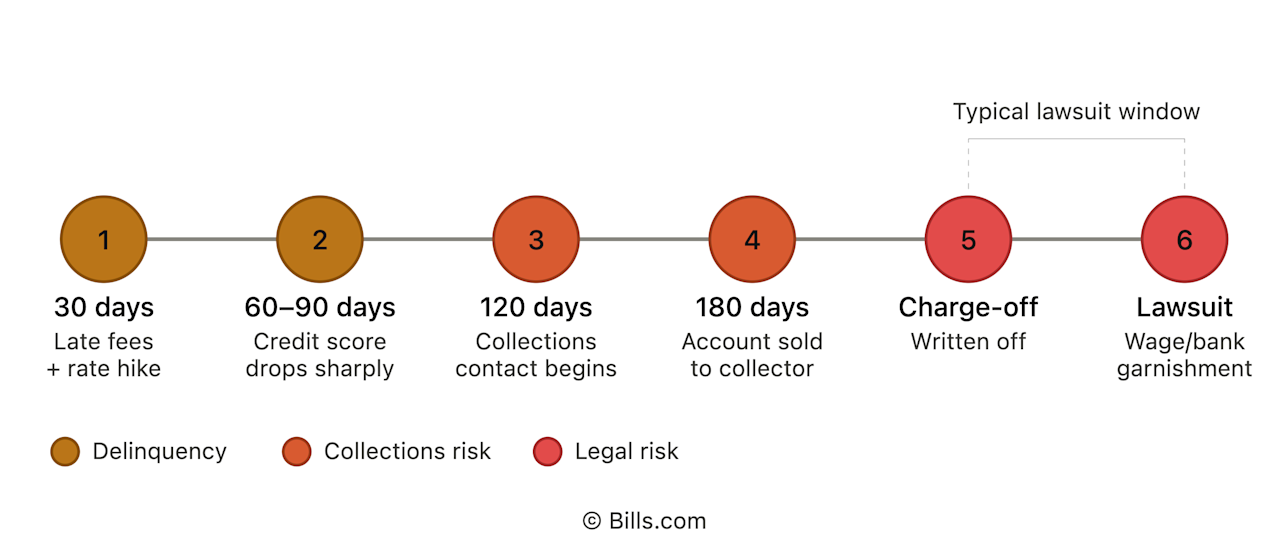

There’s no single moment when a lawsuit becomes automatic. But there is a timeline, and the most important milestone is 180 days.

At 180 days past due, federal banking regulations require credit card accounts to be charged off. This means the creditor writes your balance off as a loss for its own tax and accounting purposes. It is not forgiveness and you still owe the debt. The creditor can still collect it, sell it, or sue you for it.

Some issuers charge off accounts before 180 days. The point is the same: a charge-off often precedes a lawsuit. It does not guarantee one.

What factors make a credit card company decide to sue?

Creditors don’t sue randomly. The decision comes down to a cost-benefit calculation. Knowing what goes into it can help you read your own situation.

According to the CFPB’s 2023 Consumer Credit Card Market Report, credit card companies sued roughly 12% of customers with delinquent accounts. The average balance at the time of suit was approximately $2,700. That’s an average, not a minimum. Creditors sue for balances above and below that figure.

Several factors shape the decision:

- Your balance. A larger balance is more likely to justify the cost of litigation.

- Your communication. If you’ve stopped answering calls or sent a cease-and-desist letter, a lawsuit may be the creditor’s only remaining option. Staying in contact, even if you can’t pay, sometimes changes the outcome.

- Who holds the debt. This one matters more than most people realize. Original creditors often sell delinquent accounts to debt buyers. A debt buyer purchases your account for a fraction of the original balance. Because it paid less, it may be more willing to sue on smaller amounts than the original creditor would.

- Whether you’re judgment-proof. Being judgment-proof means you have no steady income and no seizable assets. If that’s your situation, a creditor may calculate that winning a lawsuit still won’t get it paid. That could work in your favor, though it’s not a guarantee of protection.

- Your state. Some states have stronger consumer protections that affect when and how creditors pursue legal action.

None of these factors guarantees a lawsuit or prevents one. They’re the variables that influence the situation.

What happens if a credit card company sues you?

A lawsuit doesn’t appear out of nowhere. There’s a process, and knowing the steps helps.

- Before filing, the creditor or its attorney usually sends a demand letter. It states what you owe and gives you a deadline to respond. It signals that legal action is coming.

- If no resolution follows, the creditor files a complaint with the court. The court issues a summons: a formal notice that a case has been filed and that you must respond.

- You have a deadline to file a written response, called an answer. In most states, that window is 20 to 30 days from when you were served. Deadlines vary by state and court.

- If you don’t respond, the court will enter a default judgment against you. A judgment is a court order stating that you owe the debt. The creditor simply wins because you didn’t show up.

Once a creditor has a judgment, it gains legal tools it didn’t have before:

- Wage garnishment: your employer withholds a portion of your paycheck and sends it to the creditor.

- Bank account levy: funds can be seized directly from your account.

- Property lien: a claim is placed against real estate you own.

Some states widely restrict or prohibit wage garnishment for consumer debt. Texas, North Carolina, Pennsylvania, and South Carolina are common examples. State laws vary and can change, so verify the current rules where you live.

How can you defend against a credit card lawsuit?

Being served with a summons doesn’t mean you’ve already lost. There are real defenses—but raising them requires responding to the lawsuit, not ignoring it.

- The statute of limitations. Most states give creditors three to six years to sue over credit card debt. If that window has closed, you could have grounds for dismissal. One warning: making a payment or acknowledging the debt in writing can restart the clock in many states.

- Lack of standing. Debt buyers must prove they own your debt by documenting the full chain of ownership. That documentation sometimes has gaps.

- Incorrect amount. The creditor must prove the specific balance with a transaction history. A generic statement often isn’t enough.

- Prior bankruptcy discharge. If the debt was discharged in bankruptcy, it cannot legally be collected.

Consult an attorney before your answer deadline. We can provide general information, but not legal advice.

What are your options if you’re worried about a credit card lawsuit?

The earlier you act, the more options you have. Here’s how to think about the landscape:

- Contact your creditor and ask about hardship programs. Some creditors may reduce your interest rate, waive fees, or arrange a lower payment if you reach out before charge-off. Keeping communication open tends to work in your favor.

- A debt management plan (DMP) through a nonprofit credit counseling agency keeps reduced payments flowing to your creditors and should lower the likelihood of legal action.

- Debt settlement means getting your creditor or debt buyer to agree to accept less than you owe and forgive the rest. Here is what you need to know first: enrolling in a debt settlement program involves stopping payments to your creditors. Creditors can and do sue consumers who are enrolled in settlement programs. Forgiven debt may be taxable. A tax advisor can tell you what applies to your situation.

- Bankruptcy triggers an automatic stay, which immediately stops most collection activity, including a pending lawsuit. The long-term consequences for your credit are real. It’s a decision worth making with professional guidance.

To explore your options, visit Bills.com debt relief.

Bills Action Plan

1. Check your account status. Log in or call your creditor to confirm how many days past due you are and whether the account has been charged off or sold.

2. Look up your state’s statute of limitations for credit card debt. If the clock has run out, you may have a defense before you respond to any lawsuit or collection contact.

3. Explore your options before a lawsuit is filed. Contact a nonprofit credit counselor, bankruptcy attorney, or debt relief specialist to understand what’s still available for your situation.

Key Terms

Charge-off: An accounting classification used when a creditor writes a debt off as a loss. Federal regulations require credit card accounts to be charged off at 180 days past due. It does not cancel the debt.

Default judgment: A court ruling for the creditor. It’s entered when a defendant doesn’t respond to a lawsuit by the deadline.

Statute of limitations: The legal window for a creditor to sue over unpaid debt. Most states set it at three to six years for credit card debt.

Judgment-proof: Having no income or assets a creditor could legally collect, even after winning in court.

Debt buyer: A company or individual that buys charged-off debt from original creditors for a fraction of the original balance. It then attempts to collect or may file suit. This article is for general education. Bills.com does not provide legal or tax advice. For guidance specific to your situation, consult a qualified attorney or tax advisor.

Free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Actual client of Freedom Debt Relief. Client’s endorsement is a paid testimonial. Individual results are not typical and will vary.

Can a credit card company sue you for a small amount?

Yes, though it is less common. According to the CFPB, the average balance at the time of a credit card lawsuit was approximately $2,700. That is an average, not a minimum. Original creditors may be less inclined to sue over small balances because litigation costs can outweigh what they’d recover. Debt buyers purchase old accounts for a fraction of the original balance and are sometimes more willing to pursue smaller amounts in court.

What should I do if I receive a summons from a credit card company?

Do not ignore it. In most states, you have 20 to 30 days to file a written response, called an answer, with the court. If you don’t respond, the court will enter a default judgment against you. That gives the creditor tools to garnish wages or levy your bank account. Even a brief consultation with an attorney before your deadline could help you understand your options and whether any defenses apply.